If you’ve ever looked at your charity’s year end accounts and found yourself puzzled by the terms ‘assets’ and ‘liabilities’, you’re not alone. These are two of the most fundamental concepts in accounting. And once you understand them, a lot of the rest starts to make sense.

This article explains what assets and liabilities are, why they matter for churches and charities, and how to think about them in a practical, everyday way.

In this article:

- What is an asset?

- What is a liability?

- Net assets: the big picture

- Where do you see assets and liabilities in charity accounts?

- What about charities accounting on a receipts and payments basis?

- A practical example of assets, liabilities and the balance sheet

- Fixed assets and depreciation

- How does understanding assets and liabilities help trustees?

- Summary

Estimated reading time: 9 minutes

What is an asset?

Put simply, an asset is anything your charity owns or is owed that has value.

Think of assets as things that are working in your favour – things you have that help your charity do what it does. Assets fall into two broad categories:

Current assets – things that are either already cash, or which you could convert into cash within the next year, such as:

- money in your bank account

- cash in a petty cash tin

- accounts receivable – money owed to the charity (for example, Gift Aid from HMRC)

- prepayments – money paid in advance (for example, payments of deposits or prepaid expenses)

Non-current assets – things that your charity holds for long-term use. These typically include any financial investments, as well as fixed assets, such as:

- a building or land

- furniture, equipment, or musical instruments

- vehicles like a minibus used for community work.

Learn more about accounts receivable and prepayments in this article on debtors and creditors.

What is a liability?

A liability is the opposite of an asset – it’s anything your charity owes to someone else.

Liabilities are financial obligations. They’re amounts that you will need to pay out at some point. Again, these fall into two broad categories:

Current liabilities are amounts you owe that are due within the next year, such as:

- accounts payable – money you owe (for example, wages owed to a staff member or an unpaid invoice from a supplier)

- deferred income – money received in advance (for example, ticket income for an event next year)

- a short-term loan or overdraft.

Non-current liabilities are amounts you owe over a longer period, such as:

- a mortgage on a building

- a long-term loan from a bank or funder.

Learn more about accounts payable and deferred income in this article on debtors and creditors.

Net assets: the big picture

Once you understand assets and liabilities, the concept of net assets becomes straightforward.

Net assets = total assets − total liabilities

Essentially, this is what your organisation is actually ‘worth’ once you’ve taken away everything you owe.

It’s the financial ‘health check’ of your charity – and it’s one of the first things that trustees, auditors, and independent examiners will look at.

Therefore, if your net assets are positive, your organisation has more assets than liabilities. However, if your net assets are negative, your liabilities outweigh your assets.

To learn more about financial health checks for charities, see this article on key financial metrics every UK charity should know.

Where do you see assets and liabilities in charity accounts?

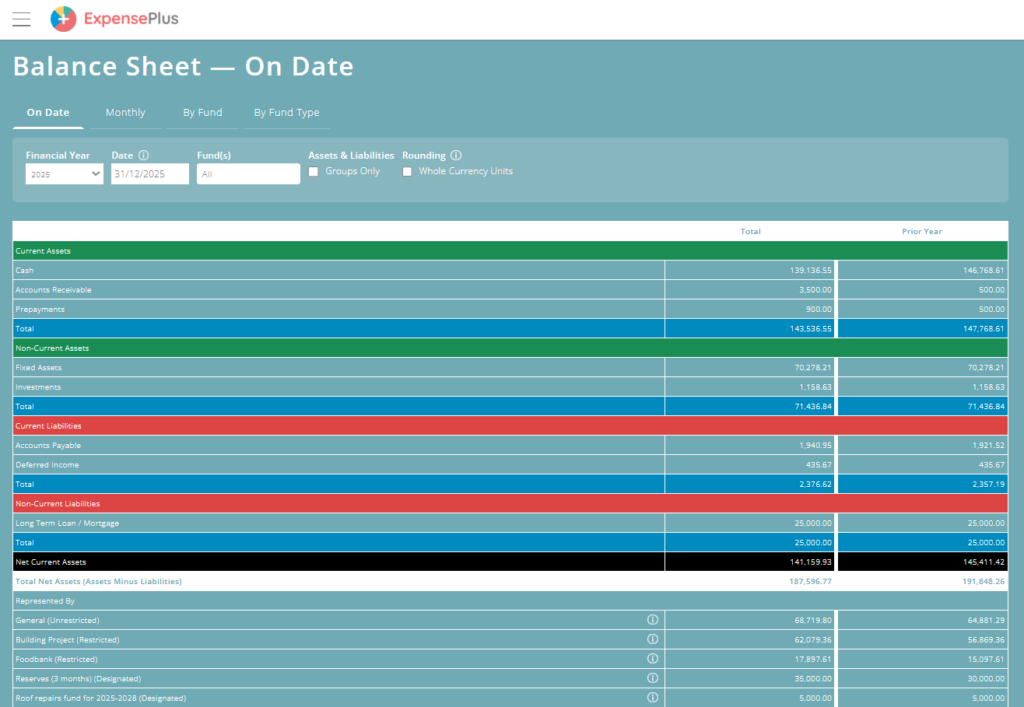

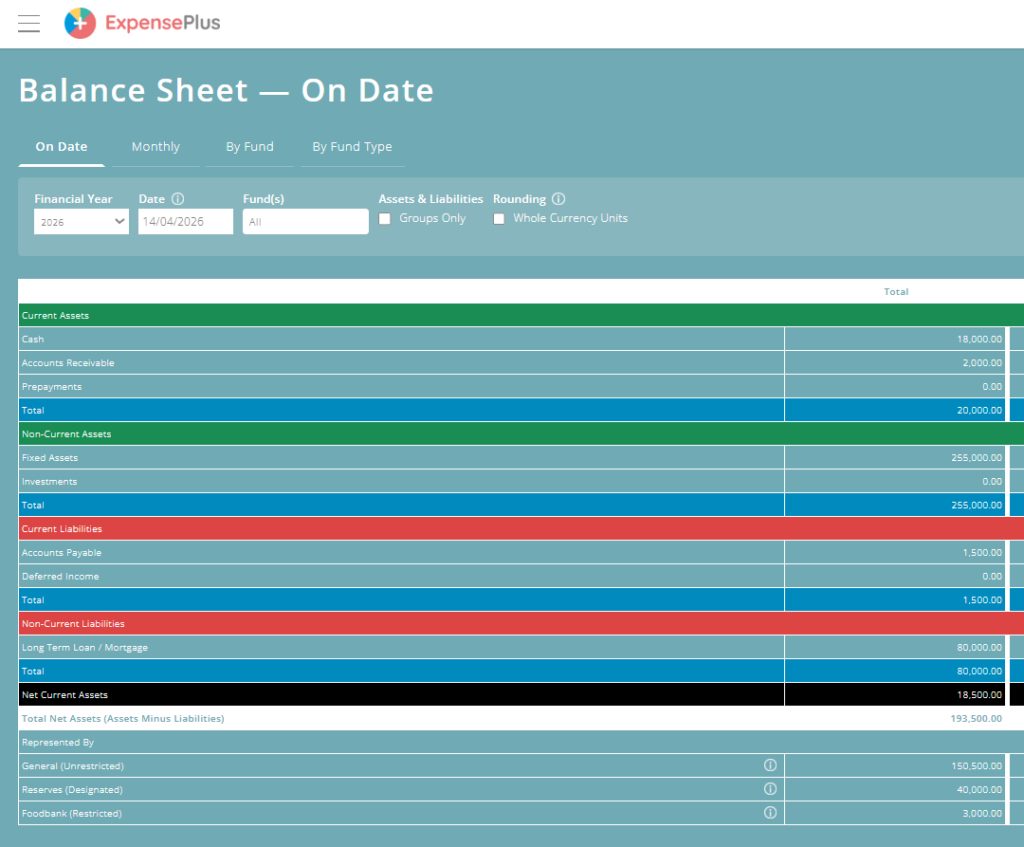

For charities that create accounts on an accruals basis, assets and liabilities appear in a report called the Balance Sheet report (sometimes called the Statement of Financial Position in charity accounts).

This report gives a snapshot of where your charity stands financially at a specific point in time – usually on the last day of your financial year.

The balance sheet shows:

- current assets

- non-current assets

- current liabilities

- non-current liabilities

- net assets (the resulting figure).

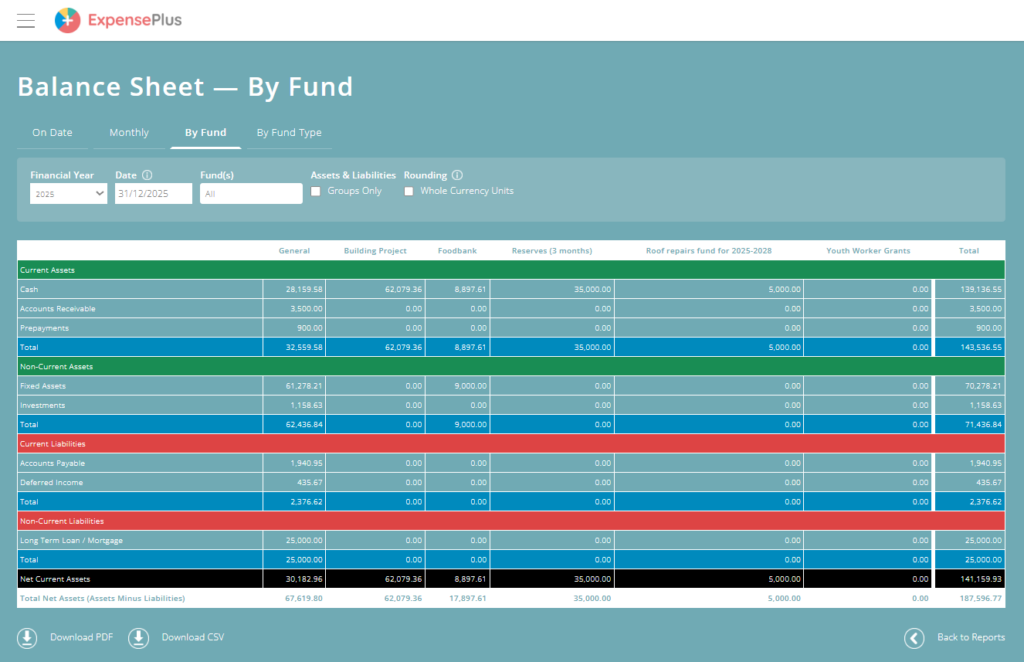

In charity accounting, an organisation’s assets and liabilities are held within different funds.

Learn more here about fund accounting for charities.

You can see the balances for each fund in the bottom section of the Balance Sheet report (in the ‘represented by’ section).

The total net assets of all funds must always equal the total net assets of the organisation shown in the balance sheet.

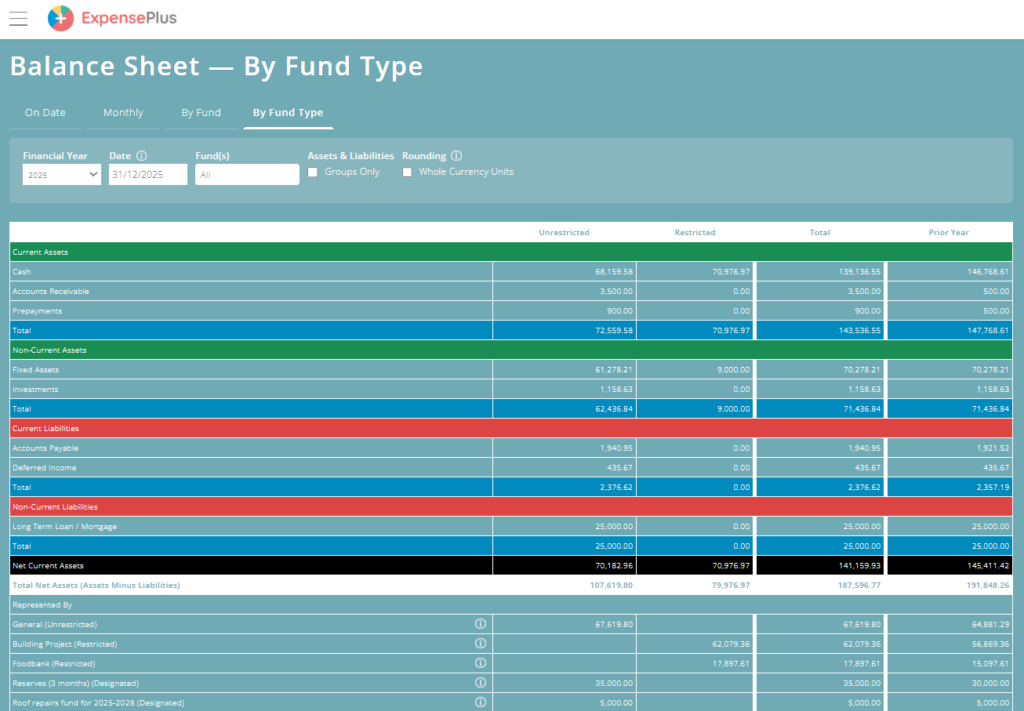

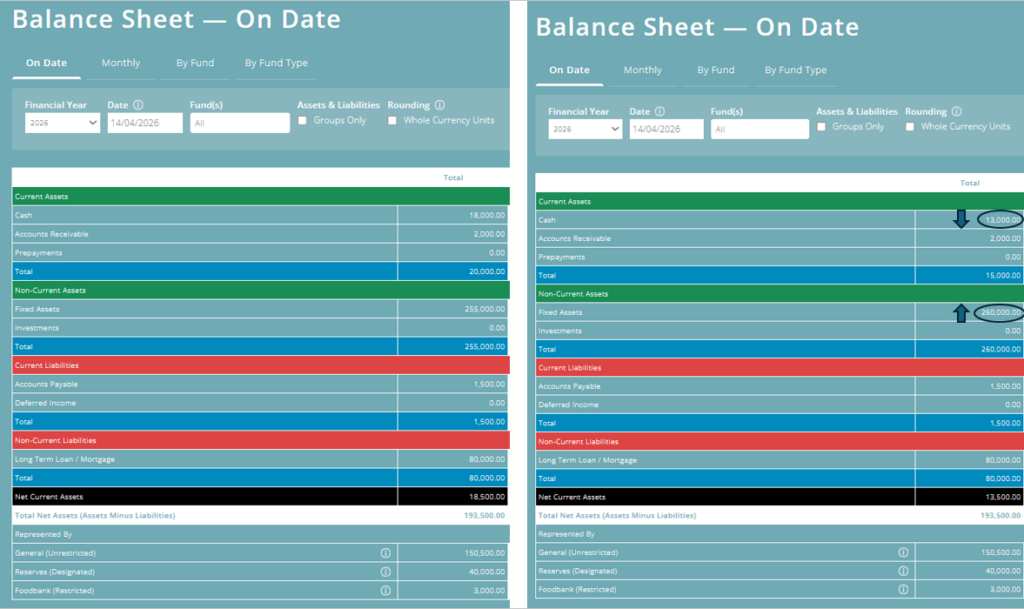

Fund accounting packages such as ExpensePlus provide different versions of the balance sheet to help you more easily understand your assets and liabilities.

These include:

- Balance Sheet by month – helps track how assets and liabilities are changing over time.

- Balance Sheet by fund – helps show the breakdown of assets and liabilities between funds.

- Balance Sheet by type – the version of the balance sheet which appears in your year end accounts.

To learn more about the balance sheet, see this article on the balance sheet in charity accounting.

What about charities accounting on a receipts and payments basis?

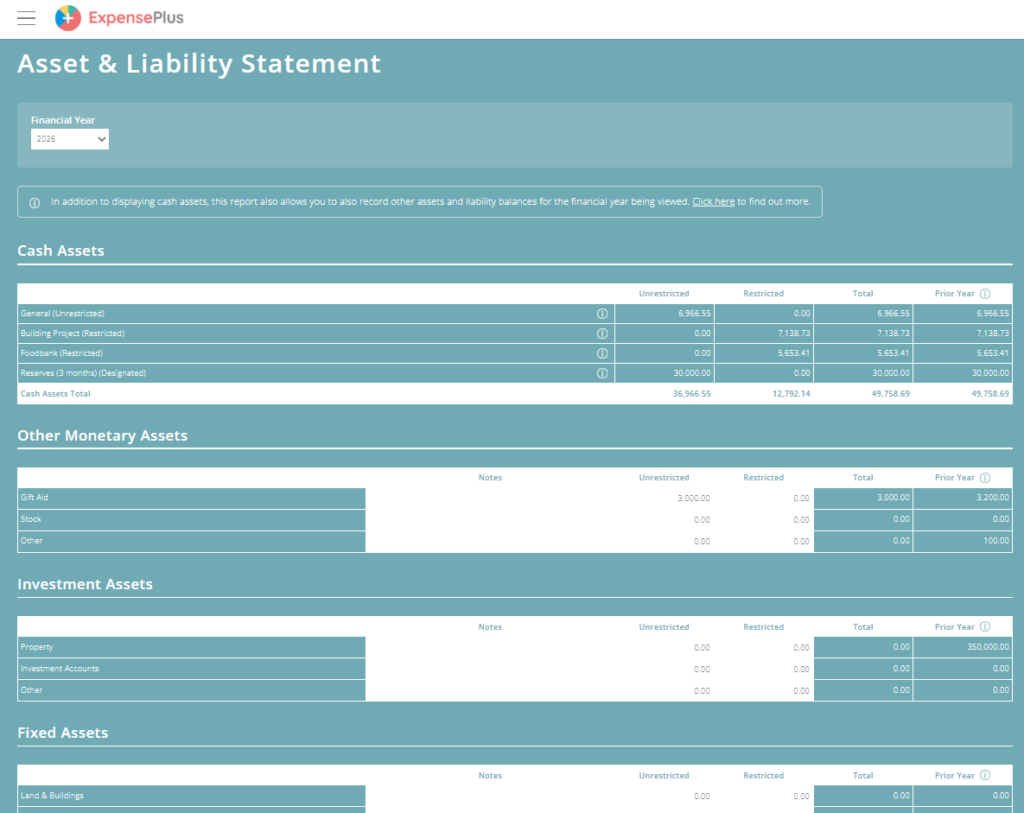

For charities that create accounts on a receipts and payments basis (also known as cash accounting), assets and liabilities appear in a report called the Assets and Liabilities Statement.

Unlike with accruals accounting, non-cash assets are simply a snapshot value, recorded at a particular point in time (usually at the end of each financial year) within the Assets and Liabilities report.

To learn more about this, see these articles on:

- Receipts and Payments vs. Accruals Accounting and

- How to create Receipts & Payments based Year End Accounts

A practical example of assets, liabilities and the balance sheet

Let us consider the example of the charity King’s Church, which creates accounts on an accruals basis. It has the following amounts at the end of its financial year:

- a building valued at £250,000 (asset)

- equipment worth £5,000 (asset)

- £18,000 in the bank (asset)

- £2,000 Gift Aid due in from HMRC (asset – a debtor)

- an outstanding invoice of £1,500 to a cleaning company (liability – a creditor)

- a long-term mortgage of £80,000 (liability)

Total assets = £250,000 + £5,000 + £18,000 + £2,000 = £275,000

Total liabilities = £1,500 + £80,000 = £81,500

Net assets = £275,000 − £81,500 = £193,500

This figure of £193,500 would show as the total funds in the charity’s accounts, split across whichever funds the charity holds.

Fixed assets and depreciation

One thing that often surprises people is that fixed assets such as buildings and equipment don’t stay at the same value in your accounts over time.

So, while you may insure these items at the price you paid for them, or at the cost to replace them, this is likely different to the value of your fixed assets shown within your accounts.

When you purchase something that qualifies as a fixed asset for your organisation, rather than showing it as expenditure, you need to capitalise it. This will mean it shows on the balance sheet as a fixed asset.

The purchase of a fixed asset doesn’t change the overall net assets of a charity.

However, most fixed assets don’t retain their value forever, so something needs to happen in order for the value shown on the balance sheet to reduce over time. This ensures that the net asset value shown on the balance sheet still accurately shows what the charity is ‘worth’.

The process of reducing the value of fixed assets is called depreciation.

For example, a laptop purchased for £1,200 might be depreciated over three years, meaning £400 is ‘written off’ each year to reflect the fact that the laptop is getting older and is less valuable. This keeps your balance sheet accurate and realistic.

Buildings are sometimes treated differently – many charities hold their buildings at historic cost (what they originally paid) or at a revalued amount, depending on their accounting policy.

To learn more about fixed assets, see this article on fixed assets in charity accounting.

How does understanding assets and liabilities help trustees?

As a trustee or treasurer, understanding your charity’s assets and liabilities helps you to:

- assess financial health – are you in a strong position, or are there potential issues?

- plan ahead – knowing what you own and what you owe helps with budgeting and reserves planning

- meet your legal responsibilities – trustees have a duty to ensure the charity’s finances are properly managed and reported

- build donor confidence – clear, transparent accounts reassure funders and donors that their money is being properly stewarded.

You don’t need to be a trained accountant to understand this. But having a basic grasp of assets and liabilities means you can engage meaningfully with your accounts and help the rest of your team do so as well.

Summary

| Term | Simple definition | Examples |

|---|---|---|

| Current asset | Something short-term or liquid | Cash, Gift Aid due in from HMRC |

| Long-term asset (including fixed assets) | Something you own long-term | Investments, building, vehicle, equipment |

| Current liability | Something you owe within a year | Supplier invoices and expenses yet to be paid |

| Long-term liability | Something you owe over the long term | Mortgage, long-term loan |

| Net assets | What your charity is ‘worth’ after paying what you owe | Total assets minus total liabilities |

Understanding assets and liabilities is key to becoming confident with charity accounting and understanding key financial reports.

With fund accounting software like ExpensePlus, figures are calculated automatically – so you can always see a clear, up-to-date picture of your charity’s finances.

Alongside the software, there is also free training to help you understand key financial reports and create accurate year end accounts.

ExpensePlus is a cloud-based fund accounting software package designed for churches and charities. ExpensePlus makes managing fund accounts simple and straightforward. It’s used by hundreds of charities and churches across the UK and is rated 4.8 stars (out of 5) on Google with over 1000 user reviews.