Understanding key financial metrics is important for all churches and charities. Key financial metrics (sometimes known as KPIs – Key Performance Indicators) provide important insights into areas such as income diversity and donor engagement.

Key financial metrics can also provide a measurable way to determine whether a charity is operating efficiently and effectively. They can help ensure the charity has sufficient cash to meet short-term obligations, as well as helping to assess the charity’s long-term sustainability.

Most charities are not short on financial metrics. The challenge is often knowing which metrics are important and what they show.

This guide covers the key financial metrics to track.

In this article:

Estimated reading time: 13 minutes

Understanding how your charity generates income is vital for your financial sustainability. You should keep track of these three important key financial metrics related to your charity’s income.

Key financial metrics: income

Surplus margin

A charity exists to deliver public benefit, not profit. However, generating a surplus allows a charity to invest in the improvement and expansion of its charitable activities, so understanding a charity’s ‘profit margin’ (or surplus margin) is important.

To calculate this, you will need to know the charity’s total income and total expenditure for the financial period (typically a financial year).

The formula used to calculate surplus margin is shown below.

In the example above:

As shown above, Surplus Margin is usually expressed as a percentage (by multiplying by 100):

If the surplus margin overall is positive, the charity has made a surplus and its reserves will be boosted. A margin of zero means breaking even.

If the margin is negative, the charity has made a deficit and is eating into its reserves. Depending on the size of the deficit, and the level of reserves, this may or may not be sustainable.

A charity’s aim will usually be to at least ‘cover its costs’ (break even).

Income sources

Understanding a charity’s income sources is important, particularly when it comes to assessing financial risk. Income sources may include:

- Donations

- Gift Aid

- Grants

- Event income

- Sales income

- Rental income

- Bank interest

- Investment returns

Where a charity has only one main source of income, this may pose considerable financial risk to the charity. For example, if this source of income were to end. This is particularly the case if the charity relies heavily on grant funding that’s primarily from one or two funders.

For many charities, diversifying income streams is a good way to mitigate against this financial risk.

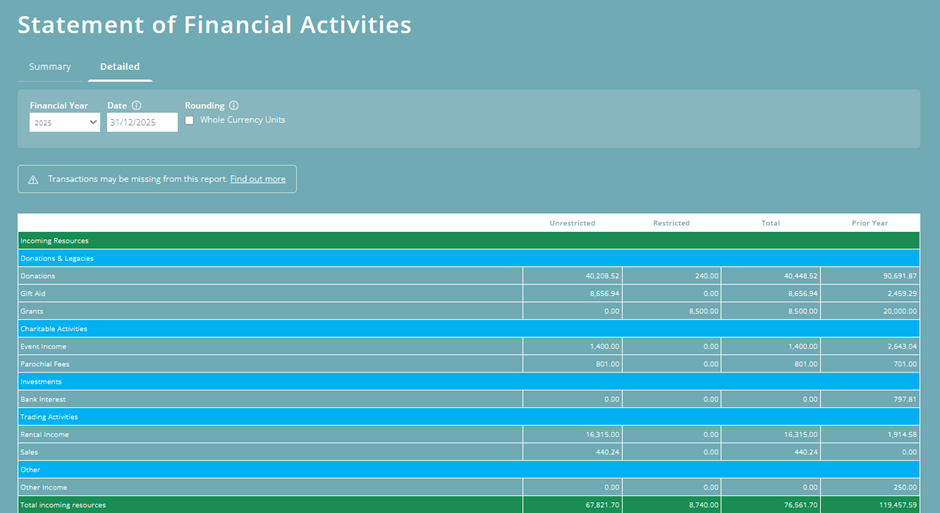

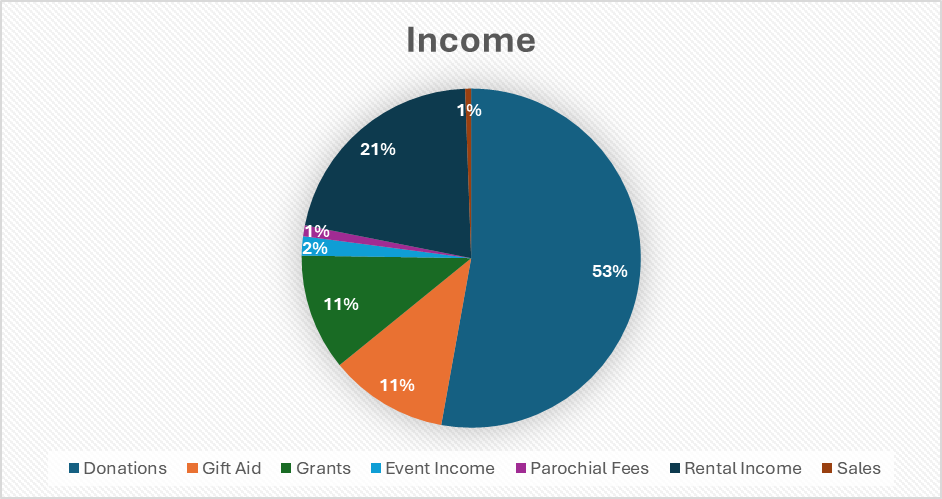

Financial reports such as the detailed version of the Statement of Financial Activities (SOFA report) can be helpful by providing a breakdown of charitable income for organisations accounting on an accruals basis. Organisations accounting on a cash basis can use the Receipts and Payments Statement.

Viewing this breakdown graphically is often really helpful, graphically, by downloading data and creating an image, for example in the form of a pie chart.

Questions for your team:

- Are you aware what percentage of your charity’s income comes from grants, rental income, donations, and other sources?

- How dependent is your charity on a particular funding source, individual or organisation?

- What would happen in terms of financial sustainability if a particular income stream stopped?

Donation statistics

If donations are a key source of income for a charity, then the chances are the charity is already working to increase the number of donors that give, as well as encouraging donors to increase the amount they give. Two ways to increase donations is to simplify the donation process and thank donors for their generosity.

There are several reasons a charity might want to increase donations: for example, to cover a shortfall in income, to cover rising costs, to help diversify the charity’s income, or to improve or expand existing charitable activities.

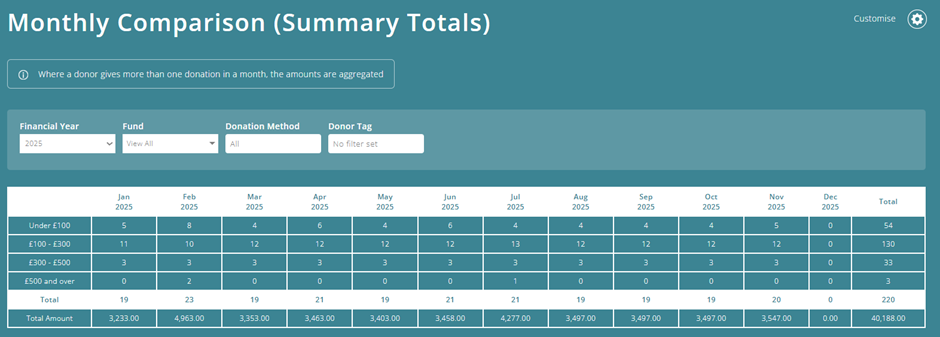

Gaining an understanding of donor giving is really important. Being able to view this breakdown month on month is a really helpful metric, as it can make it easier to identify trends and track how successful a charity has been at increasing the donor numbers and how much donors are giving. If you are using a charity accounting package, then you should be able to view this information at the click of a button, with reports such as the donor summary report within ExpensePlus.

Where the donations of a small number of individuals make up a large proportion of a charity’s income, this is likely to pose a key risk to that charity. For example, if those donors were to decrease or end their giving.

Questions for your team:

- Are you tracking your charity’s donor statistics?

- How successful has your charity been at increasing the number of donors and the amount donors give?

- Do you have one or two large donors?

- What would happen in terms of financial sustainability if a particular donor stopped giving?

Key financial metrics: expenditure

Understanding how your charity spends money is important, particularly when it comes to the question of financial sustainability. You should keep track of these two important key financial metrics related to your charity’s expenditure.

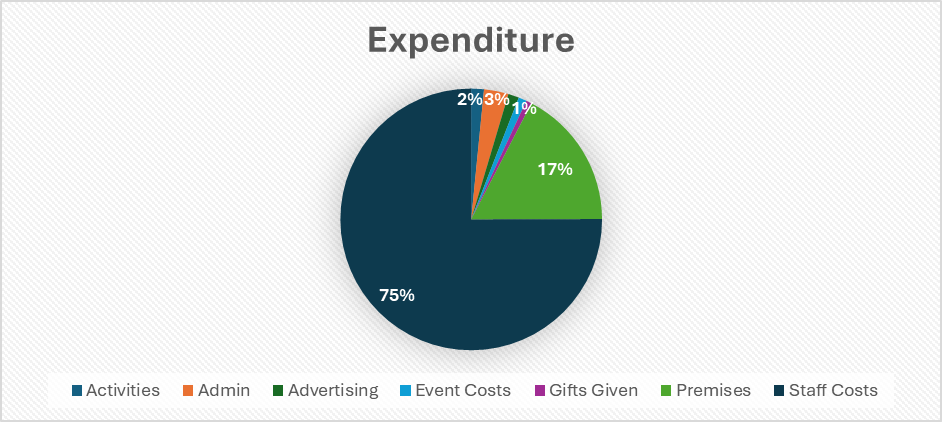

Expenditure breakdown

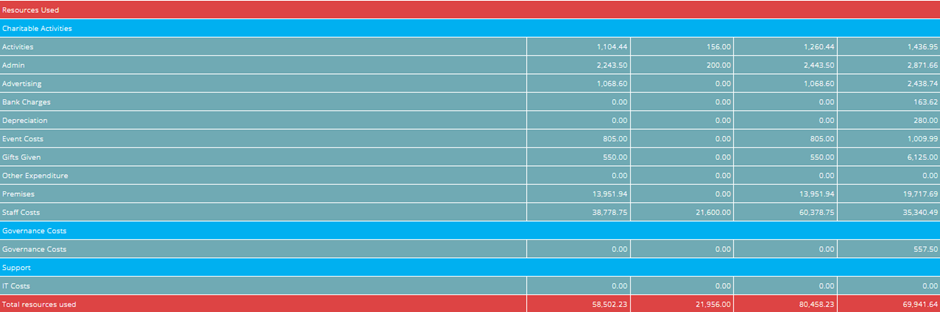

Understanding the breakdown of a charity’s expenditure is an important metric.

Financial reports such as the detailed version of the Statement of Financial Activities (SOFA report) can be helpful by providing this breakdown for organisations accounting on an accruals basis. Organisations accounting on a cash basis can use the Receipts and Payments Statement.

However, note that if your charity creates accounts on an accruals basis, this report only shows expenditure. It does not include other costs such as loan repayments, mortgage repayments or fixed asset purchases, which may also need to be taken into consideration.

It can often be helpful to view the breakdown graphically, by downloading data and creating an image, for example in the form of a pie chart. Your charity might consider how to reduce costs and how it keeps track of spending using purchasing policies.

Employment cost ratio

Adequate spending on staff and operations is essential for a charity’s effectiveness, sustainability, and ability to deliver on its mission.

Not spending enough on staffing can lead to a variety of problems. These might include the charity operating inefficiently, being unable to deliver effective services, employees being overworked, feeling stressed, poor morale, or higher turnover of staff.

On the other hand, spending too much on staffing can cause financial challenges, particularly with rising employment costs alongside other cost increases.

It’s important that staffing expenditure is sustainable, and that sufficient finance is also available for non-staffing related costs. To calculate the employment cost ratio, take the total employment cost, divide this by the charity’s total expenditure, then multiply by 100.

In the above example:

Questions for your team:

- What percentage of your charity’s expenditure goes toward staffing?

- How has this changed compared to previous years?

- Is the number of staff you employ sustainable?

Key financial metrics: cash and reserves

Understanding a charity’s reserves is essential for the charity’s smooth operation. We’ve included the two most common key financial metrics on cash and reserves and how to calculate them.

Liquidity cover

This metric is a useful measure that shows how many months of operations a charity can afford with its current unrestricted cash in hand if there were a sudden loss of income.

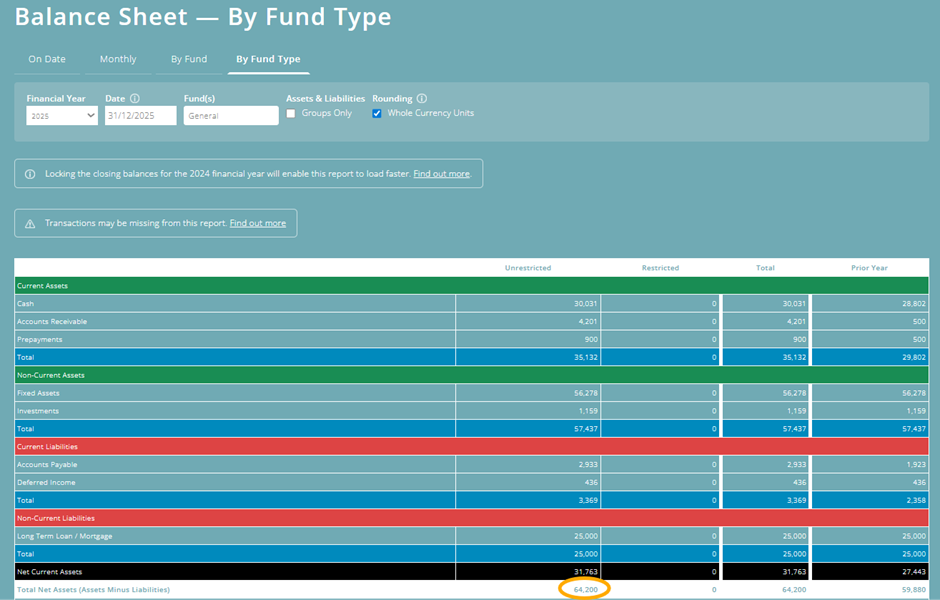

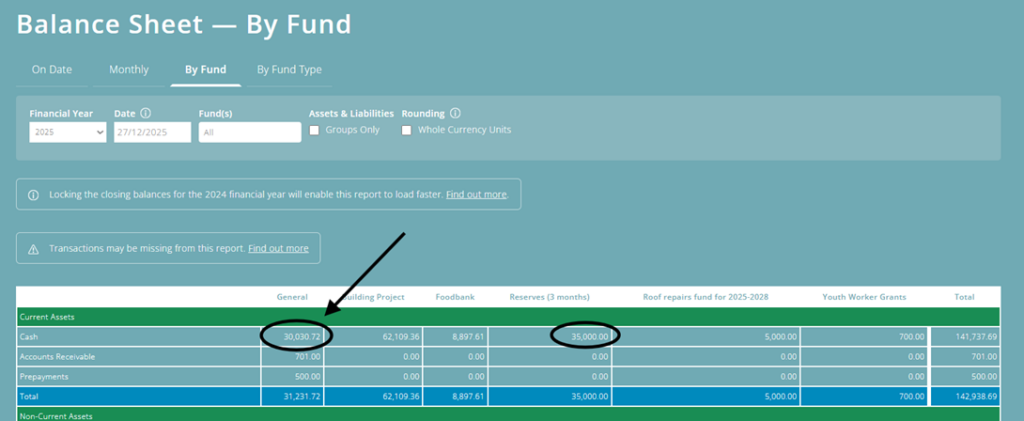

To calculate this metric, you will need to know the charity’s Unrestricted cash in hand. This figure is easy to find on the charity’s balance sheet by fund report (if accounting on an accruals basis) or your Assets and Liabilities Statement (if accounting on a receipts and payments basis).

This calculation should include designated funds, which are a type of unrestricted fund.

You will also need to calculate:

For example:

The formula to calculate liquidity cover is:

In this example:

In this example, the charity has roughly 3.5 months of cash in hand.

Free reserves

An alternative metric to use is free reserves.

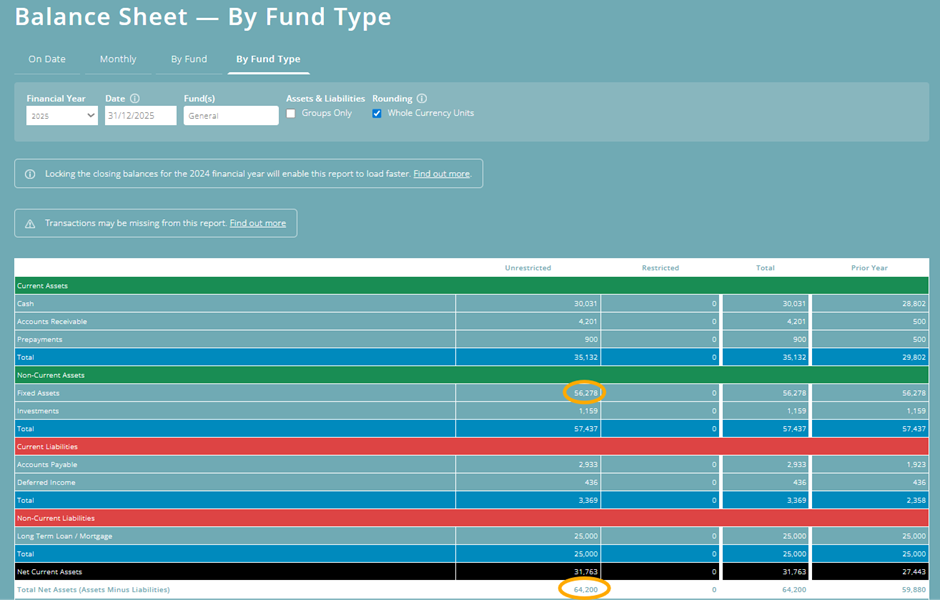

To calculate this metric, you will need to know the amount of Unrestricted Net Assets held by the charity.

This figure is easy to find on your charity’s balance sheet by fund report (if accounting on an accruals basis) or your Assets and Liabilities Statement (if accounting on a receipts and payments basis).

This calculation should include designated funds, which are a type of unrestricted fund.

However, some of the charity’s unrestricted funds may not be readily available for spending, because spending these funds would adversely impact the charity’s ability to deliver its aims.

An example of this is Fixed Assets. For example, if the charity were to sell its building, minibus, laptops etc., this would adversely affect its ability to continue delivering its aims and objectives.

Therefore, Fixed Assets are subtracted from the Unrestricted Net Assets when calculating free reserves.

The formula to calculate free reserves is:

In this example:

You may also need to make further deductions for:

- any designated funds set aside to meet essential future spending, such as funding a project that cannot be met from future income

- any financial commitments that aren’t shown on your balance sheet (and therefore haven’t been included as liabilities on your balance sheet).

Reserves policy

It is recommended that charities have a reserves policy. A reserves policy states the amount of money the trustees aim to hold in reserve.

It’s up to each charity to set its own reserves policy, and this will vary between charities.

For many charities, the reserves are held in a separate designated fund, as it’s often a helpful way to ensure that sufficient funds are held in reserve, should they be needed.

It also makes it easy to view the amount of free reserves the charity has, over and above the amount of reserves set aside.

Typically, charities should review their reserves policy at least annually. Where a charity has a separate reserves fund, it’s important to recalculate average monthly expenditure at least annually, as costs may have increased (or decreased).

Once this calculation has been made, a charity would then move money between funds so that the reserves fund reflects the amount set out by the policy.

A charity holds reserves to ensure continuity in several scenarios – for example, if its income reduces, or funding doesn’t come in as expected, or to cover any unexpected costs, or for emergencies.

Holding sufficient reserves also provides donors and grant funders with confidence that the charity is financially secure, and is being well-managed.

Questions for your team:

- How much does your charity hold in cash reserves?

- Does your charity have a reserves policy?

- Do you hold the level of reserves set out in your reserves policy?

- Do you have a separate designated reserves fund to help ensure that sufficient money is set aside as reserves?

Further resources

- Creating a Budget – A Practical Guide for Churches and Charities

- Understanding Key Charity Financial Reports

- Financial Risk Management for Charities and Churches

- How much should our charity hold in reserve?

ExpensePlus is a cloud-based fund accounting software package designed for churches and charities. ExpensePlus makes managing fund accounts simple and straightforward. It’s used by hundreds of charities and churches across the UK and is rated 4.8 stars (out of 5) on Google with over 1000 user reviews.