Charities in England and Wales with an annual income below £250,000* (this will be increasing to £500,000 for financial years ending on or after 30th Sept 2026) can often prepare Receipts and Payments based year end accounts (unless they are charitable companies).

With the right software, creating year end accounts on a Receipts and Payments basis doesn’t have to be complicated.

Whether you use accounting software or a spreadsheet to manage your finances, this blog provides a step-by-step guide for how to create year end accounts on a Receipts and Payments basis.

It includes:

- A checklist of 10 key year end checks

- Guidance on how to use a template to create year end accounts

- Information on Independent Examination and submitting accounts

How long do charities have to file accounts?

You have up to 10 months after the end of your financial year to file accounts with the Charity

Commission. In this time you will need to:

- Prepare your accounts

- Allow time to write the Trustees’ Report

- Have your Independent Examiner review your accounts

- Allow time for sign-off and submission of your accounts

So, it’s best not to leave starting your accounts until the last minute!

Note: If your charity’s accounts are filed late, this will be shown on the Charity Commission website. It is likely to put off potential future grant funders and raise governance questions for anyone viewing your accounts.

Receipts and Payments based Accounts

Receipts and Payments accounting is a simplified form of accounting. Money is accounted for based simply on the date it is received in or paid out of a bank or petty cash account. This type of accounting is sometimes also referred to as cash-based accounting.

Example: Gift Aid income received from HMRC is accounted for based on when it arrives in the bank account (not based on which financial year it relates to).

The limitation of Receipts and Payments accounting is that you cannot track fixed assets, loans, investments, or creditors and debtors as you would if you were creating accounts on an accruals basis. However, the big benefit of Receipts and Payments accounting (particularly for smaller charities) is that it is simpler to understand, and much easier to create year end accounts. Independent Examination costs are typically lower as well.

See these blog posts to find out more about:

- Receipts and Payments vs. Accruals Accounting

- Independent examination and the relevant reporting thresholds

- Accruals based year end accounts

Top Tip: In Receipts and Payments accounting, income and expenditure appear in your accounts based on when the money comes into / goes out of your bank account. So, as you come towards the end of your financial year, to ensure that income and expenditure appear in the financial year that it relates to as far as possible, you may wish to: claim any Gift Aid; chase outstanding customer invoices; encourage people to submit expense claims; and pay any invoices owed before the end of your financial year.

10 key year end checks for receipts and payments

Before creating year end accounts, you need to ensure that the financial year you are creating accounts for is complete. You should check that all of the information is correct.

To help you do this, use this checklist of the key tasks. Once these checks are complete, creating year end accounts is quick and easy.

1. Opening Fund Balances

Closing fund balances from the prior financial year become the opening fund balances for the next financial year. It is therefore important to check that your opening fund balances in your accounting software or spreadsheet match the fund balances stated in your prior year accounts submitted to the Charity Commission. If they don’t, the accounts you are creating will be incorrect.

Note: If you are trying to use a business accounting package like Sage, QuickBooks or Xero to create charity accounts, it’s worth keeping in mind these packages aren’t designed for charities. Business accounting packages work on accruals basis rather than Receipts and Payments basis. These packages don’t have the concept of funds and reporting is different too. This makes tracking fund balances problematic and creating year end accounts more difficult.

Top Tip: You can download a copy of your submitted accounts for your prior year from the Charity Commission website. Just search your charity name or charity number and select the charity. Then select the ‘Accounts and annual returns’ option on the sidebar menu.

2. Bank Transactions

Since Receipts and Payments accounting is bank statement driven, it’s important to ensure all bank transactions have been included and reconciled, as either income (receipts) or expenditure (payments).

If you are using a fund accounting package like ExpensePlus that has automated bank feeds, or if you download bank transactions as a .CSV file and upload these to your accounting software, then you are less likely to have gone wrong. If you manually key in bank transactions, there is a greater risk that there will be missing or incorrectly entered bank transactions.

Either way, at year end you need to check that bank transactions are not missing from the accounts you are creating. An easy way to check this is to compare your balances on your actual bank statements against your balances at year end according to the accounting software or spreadsheet.

If there is a discrepancy, you will need to investigate further to find out which bank transactions are either missing or duplicated and fix any issues.

You also need to check that all bank transactions have been reconciled as either income or expenditure, or bank transfers as appropriate.

Top Tip: Your Independent Examiner should request to see all bank statements for the financial year in question. So, it’s worth downloading these from your online banking in .PDF form, ready to send to your examiner.

3. Petty Cash Accounts

If you have petty cash accounts, then you need to ensure that all petty cash transactions have been recorded.

Note: All income and all expenditure need to be recorded (not just net income).

A good fund accounting package should have an inbuilt petty cash feature. This will allow those managing petty cash to record petty cash income and expenditure during the financial year. If you keep petty cash records on paper, then you will need to key in all of your petty cash transactions.

Once all of your petty cash transactions have been entered into your fund accounting software or spreadsheet, you should check that the petty cash balances at the end of the financial year match the actual physical cash you hold.

If there is a discrepancy you will need to investigate further. Where transactions haven’t been recorded, you will need to add them. Where required, you may need to add a miscellaneous income / expenditure transaction to correct the difference.

Top Tip: Accurate recording of petty cash is often problematic. If this is the case for your church or charity, you may wish to consider alternatives to petty cash. For example, digital expenses software means staff and volunteers can submit expense claims easily online and get paid back faster (removing the need for petty cash payments).

4. Purchase Receipts

Where purchases have been made, retaining receipts and invoices is a key part of keeping proper financial records. Your Independent Examiner should check receipts as part of their examination of your accounts.

If you are using a fund accounting package like ExpensePlus, then receipts are digital and can either be uploaded, photographed or emailed as part of a streamlined digital process flow. Staff and volunteers use this process flow to claim expenses, record invoices, and submit business card purchases.

Not only does this save time, paper and money, but it also removes the need to file paper records. At year end, you can simply give your Independent Examiner access to your cloud-based ExpensePlus account to view receipts digitally.

Note: There is no requirement to keep physical receipts and invoices if they are stored digitally.

If you are keeping paper-based receipts, speak to your Independent Examiner about how they will review receipts. For example, they may request a sample of receipts to be sent to them.

Your Independent Examiner will likely want to understand the processes and controls you have in place for purchase approvals and payments. They will also check that proper records are being kept and monitor how many receipts have been lost. Using a fund accounting package with an inbuilt expenses and payments process flow with digital receipts helps with this. It also provides visibility of purchases without receipts.

5. Income Documentation

As well as keeping documentation for purchases you make, you also need to keep any invoices that you have created and sent to customers.

Whilst most donations and other income won’t require documentation, you will need to keep documentation for any grants, legacies and large donations you receive. Again, your Independent Examiner should ask to see these to check for any conditions or restrictions attached to this income, and to ensure it has been correctly accounted for. For example, they will check if a restricted fund was created to allocate restricted grant income. Find out more about fund accounting and the purpose of funds.

With a fund accounting package, you can easily view which income transactions require documentation and attach documents digitally to those transactions.

Note: In addition to income documentation, your Independent Examiner may also wish to review records of bank deposits. If you use a fund accounting package like ExpensePlus they will also be able to access these as a digital record.

6. Recording of Transactions

It’s important to ensure that all transactions have been recorded correctly before you create your end-of-year accounts. If, like most churches and charities, you check your financial reports each month as you create internal finance reports, then this step probably won’t take too long.

How you perform this check will depend on which fund accounting package or spreadsheet you use. The disadvantage of a spreadsheet is that it is prone to produce errors.

You may wish to review how each bank transaction has been reconciled and/or view income and expenditure reports to identify anything unexpected that needs further interrogation.

If you have a fund accounting package like ExpensePlus, then these checks are easy to do. You can drill into reports and view transactions and receipts at the click of a button.

Note: A fund isn’t the same as a bank account. Therefore, the fund a transaction is recorded to is not based on the bank account a transaction comes into or goes out from. Find out more about fund accounting.

Whilst you may wish to check that all transactions are recorded to the correct category within a fund, it’s far more important to focus on transactions that may have been recorded to the wrong fund.

Three things you should particularly look out for are:

- Restricted Income that has been incorrectly recorded to an unrestricted fund – A question to ask yourself when deciding whether income is restricted is, “Could we spend this money on anything we choose?” (as long as it is within our overall charitable objectives). If the answer is “no” (e.g. because the donor/grant said they wanted it to be used for [a given purpose]), then the income should be accounted for as restricted income (and not allocated to your general fund).

- Expenditure within each restricted fund is not appropriate for the restrictions of that fund – For example, if you received income to run a foodbank, you can’t be allocating expenditure that is outside of what the donation or grant was given for (unless you get written permission from all donors/grant funders to do so).

- Expenditure recorded to the General fund that can be allocated to one of your restricted funds – You want to be ‘using up’ your restricted funds first (where it falls within the restrictions of the money given). Therefore, you should only allocate expenditure to your General fund if there isn’t an appropriate restricted fund that can cover the expenditure.

Note: If your charity has multiple bank accounts, transfers between bank accounts need to be recorded as bank-to-bank transfers. They should not be recorded as expenditure from one bank account and income into the other bank account as this would result in income and expenditure being wrongly overstated.

7. Fund Transfers

If you have added any fund transfers, you need to check that these have been recorded correctly. You may also need to add fund transfers.

For example, if you have a designated reserves fund (as many charities do), your trustees might decide to set aside an additional amount of money from your General fund to increase the level of reserves your charity holds. This would require a fund transfer from your General fund to your reserves fund.

Fund transfers are typically never from a restricted fund into another fund. The only exception to this would be if a donor or grant funder has given written permission for their donation to become unrestricted and used as general funds. Instead, you should code relevant expenditure to the restricted fund.

If you are unsure, then you should ask your Independent Examiner, who should be able to advise you.

8. Category Transfers

If you have recorded category transfers, you need to check that these have been recorded correctly.

For example, if you choose to set aside 10% of your general donation income to go towards a specific purpose or project e.g. to support other charities or individuals (within your charity’s charitable objectives), then you may wish to record this using a monthly income category transfer from your general fund to the appropriate designated fund.

Or perhaps your charity runs a foodbank that operates as a separate fund, and it’s been agreed that they will pay £200 per month towards rent and utility costs. Then a monthly expenditure transfer would be a common way to account for this.

Note: It’s important that category transfers are only ever between income and income categories or expenditure and expenditure categories. They should never be between expenditure and income categories, as this would result in you wrongly overinflating your charity’s income and expenditure.

If you use ExpensePlus as your fund accounting package, then it’s not possible to make a transfer from an expenditure category into an income category. However, most accounting packages don’t prevent you from doing this. This means you need to check yourself that this hasn’t happened, otherwise your accounts could be wrong.

Note: In a similar way, if you would usually send invoices, such as to groups for using your building, it is important to differentiate between those from your own legal entity or not. For example, if the group in question is part of your own legal entity (e.g. a foodbank), it’s important to account for any money paid from the foodbank fund to the general fund as an expenditure category transfer. Otherwise, you will also wrongly overinflate your overall charity’s income and expenditure.

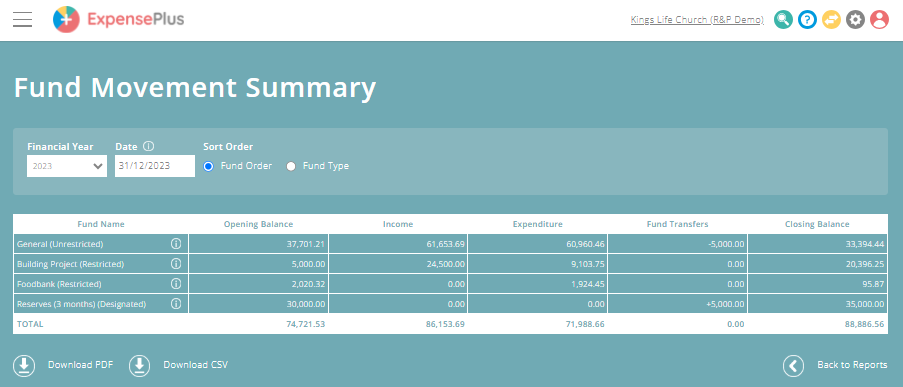

9. Check Fund Closing Balances

We’ve already mentioned in step 1, that fund balances carry over between financial years, and therefore it’s really important to ensure that your closing fund balances are correct.

If you are using a fund accounting package, then the best way to do this is to use the Fund Movement Summary report, which will provide a brilliant summary of:

- The opening balance for each fund at the start of the financial year

- The total income for each fund during the financial year

- The total expenditure for each fund during the financial year

- Any fund transfers during the financial year

- The closing balance for each fund at the end of the financial year

This will give you a final opportunity to sense-check that you didn’t miss anything in step 6 when checking transactions were recorded correctly. It will also allow you to check the closing fund balances that will be carried forward into the future financial year.

For restricted funds, here are some things to watch out for:

- Where a restricted fund has little or no expenditure during the financial year – you might want to check that there isn’t any expenditure that could have been allocated to this fund that has instead been recorded to the General fund. Remember, you want to ‘use up’ your restricted funds first; where this is within the restrictions of the money given.

- Where a restricted fund balance is running low – if you are continuing the project or activity this relates to, then you may wish to apply for more grants or ask for additional donations, or plan for expenditure to come from your general fund when the restricted fund is used up.

- Where the project relating to a restricted fund has ended – you might need to communicate with the grant funder or donors about this or think about how you can use the money in another way that is still within the restrictions for which it was given.

Note: Remember, you need donors’ / grant funders’ written permission to either change the restrictions on the money given or to transfer money to be unrestricted for general use.

Typically, no funds should end the financial year with a negative balance. The exception to this is when you are awaiting income due in e.g. a grant that is about to come in. Where a fund has a negative balance, typically you will need to either:

- Re-code some of the expenditure currently allocated to the fund to a different fund (e.g. the general fund), to prevent the fund balance from being negative, OR

- Add a fund transfer (see step 7) to get the fund balance back to zero, e.g. transferring money from your general fund to the fund with the negative balance.

If you are unsure, then you should ask your Independent Examiner who should be able to advise you.

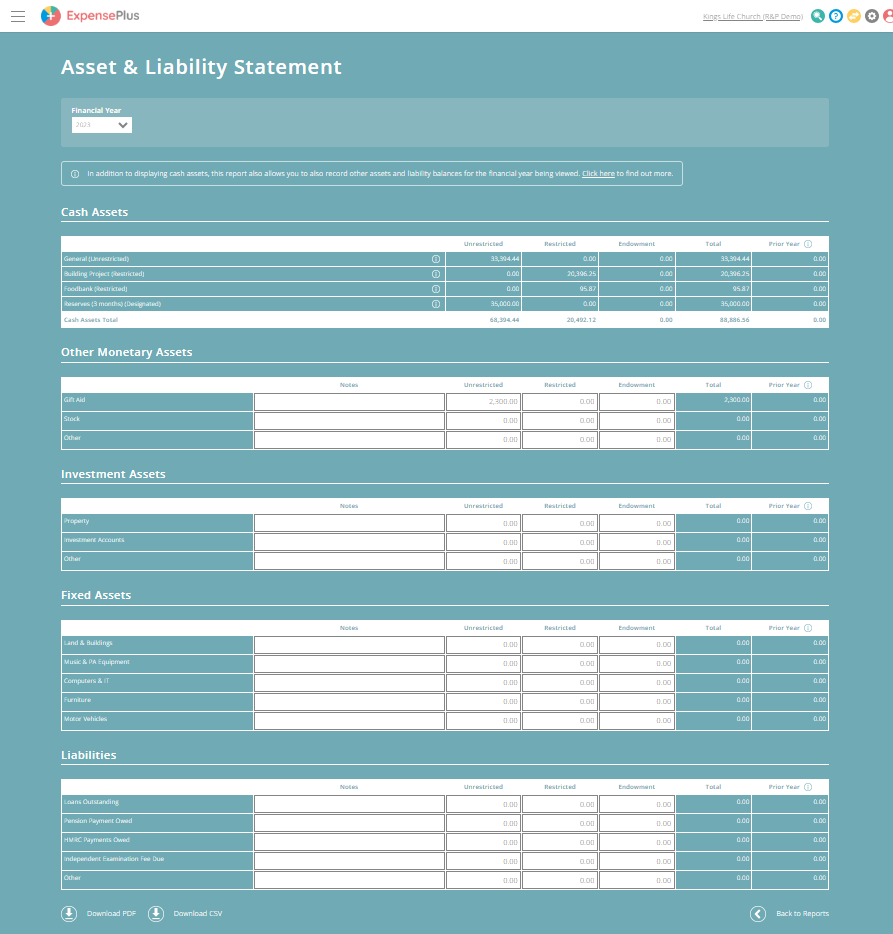

10. Add additional Assets and Liabilities

As well as cash balances, at year end you can also state your charity’s other assets and liabilities within your Asset and Liability Statement. If you are using a fund accounting package like ExpensePlus, then you can record this within the software. Otherwise, you will need to hold off on this step until you create your accounts.

The Asset and Liability Statement typically consists of:

- Cash Assets – these are the end-of-year cash balances of each of your funds (as per step 9)

- Other Monetary Assets – any Gift Aid due in or stock held at the end of the financial year

- Investment Assets – any property owned or money invested

- Fixed Assets – the value of any buildings, vehicles, equipment owned

- Liabilities – any loans and any money you owe at year end e.g. PAYE and pension payments relating to the last month of your financial year, supplier invoices that still to be paid, the independent examination fee due for examination of your end-of-year accounts etc.

The assets and liabilities in Receipts and Payments accounting work very differently compared to accruals accounting.

For example, fixed assets in accruals accounting are capitalised and then depreciated over the useful lifetime of the asset. In contrast, in Receipts and Payments accounting, an asset purchase is recorded as expenditure and the current estimated value of the asset is simply stated on the year end Asset and Liability Statement.

Another example would be money you owe at year end. In accruals accounting, as well as the money appearing as a liability on the balance sheet (similar to the Asset and Liability Statement), the expenditure also appears within the same financial year the expenditure relates to. Whereas, in Receipts and Payments accounting, it only appears on the Asset and Liability Statement.

In Receipts and Payments accounting, you simply state asset and liability balances at a given point in time (as at the end of each financial year).

Note: The principle of ‘materiality’ within accounting means that you don’t need to spend lots of time trying to add up and account for small expense claims that were owed but not paid out before year end. You also don’t need to worry about trying to include the value of the 6-year-old laptop you have in your office as a fixed asset. Your focus should be the key assets and liabilities. It’s worth being mindful that for many charities, this may mean that nothing needs adding to your Asset and Liability Statement. If you are unsure, then you should ask your Independent Examiner who should be able to advise you.

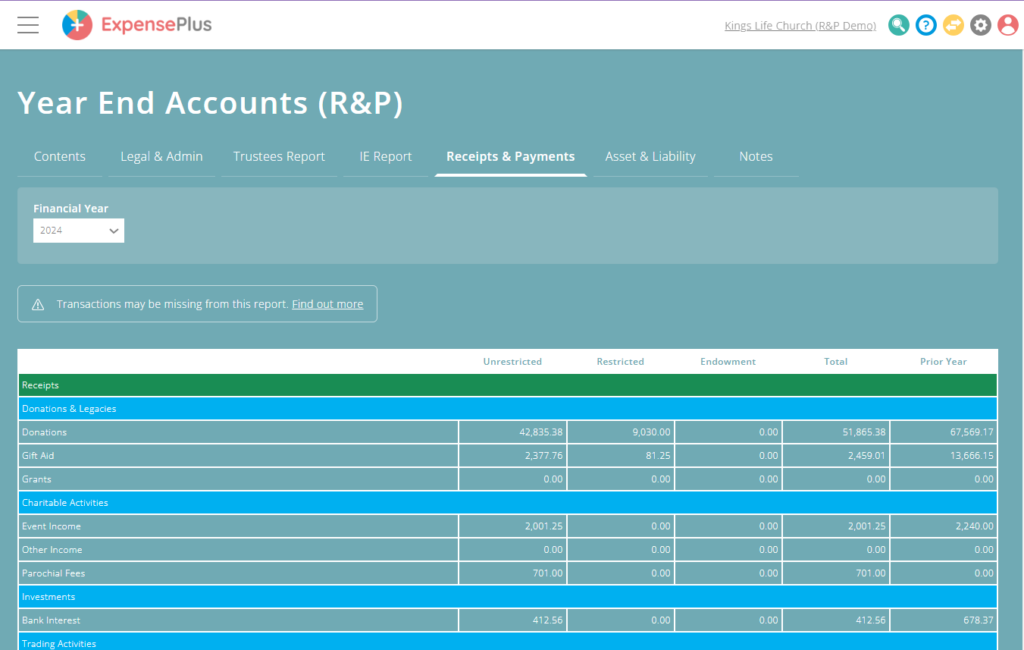

Using a Template to Create Year end Accounts

Once you have completed the checklist, creating year end accounts is quick and easy. You don’t need to be a trained accountant to prepare year end accounts. For many smaller charities, year end accounts are often prepared by a volunteer Treasurer.

Receipts and Payments accounts are a simple form of accounting that consists of a summary of all monies received and paid via the bank and in cash by the charity during its financial year, along with a summary of cash balances (and any other asset/liabilities) at the end of the financial year.

Basic Charity Commission Template

You can download and use a free Receipts and Payments accounts template from the Charity Commission website, which you can then use to prepare your accounts.

If you only have cash assets to include, then you can simply:

- Enter a summary of your income for the year in section A1

- Enter a summary of expenditure for the year in section A3

- Enter your end-of-year fund balance totals in section B1

For details of other assets and liabilities you may wish to include, see step 10 in the checklist above. Additional notes on how to complete the template can be found on the Charity Commission website.

More detailed Accounts Template

Whilst there is no requirement to do so, many charities use a more detailed accounts template than the basic one provided by Charity Commission.

If you use a fund accounting package like ExpensePlus, then a more detailed accounts template is inbuilt. All of the accounting information automatically populates into the accounts template, so you don’t need to spend time finding, copying and pasting data.

Alternatively, Independent Examiners like Stewardship provide a more detailed free accounts template for their clients to use.

For an additional fee, some Independent Examiners may also offer the option of preparing your accounts for you. However, typically this isn’t needed for receipts and payments year end accounts. If you want an easy way to create accounts, then it might be better to invest in software like ExpensePlus that will simplify the process and guide you step by step through what you need to do.

Trustees’ Annual Report (TAR)

In addition to the information in the accounts template, your accounts need to include a Trustees’ Annual Report. This is a written report that contains details of, objects of the charity and a summary of the charity’s main activities and achievements.

The Trustees’ Annual Report doesn’t need to be very long, typically 2 to 3 pages is more than sufficient. Rather than writing the report from scratch each year, many charities simply update 2 to 3 paragraphs in the report to reflect any changes, achievements or highlights that have happened in the financial year. Largely, the main activities of most charities won’t change year on year, nor will its objectives.

Remember, the Trustees’ report should be written with the audience in mind. Typically, it will only be seen by:

- Your charity members (as part of presenting the account at your AGM)

- Potential grant funders (who are likely to view your accounts on the Charity Commission website)

Your Trustees’ Annual Report is unlikely to be the main way you look to communicate the activities, achievements, and needs of your charity to your wider audience of donors and supporters.

Once you’ve prepared your accounts and written your Trustees’ Annual Report, you are ready to move onto the final stage of submitting accounts (see next section).

Top Tip: If you are using fund accounting software, then it’s worth locking the financial year you have created accounts for to prevent any changes. This avoids the balances in your accounting software no longer matching your submitted accounts.

Independent Examination and Submitting Accounts

In this section, we will cover:

- Independent examination

- Signing of accounts, and

- Submitting accounts to the Charity Commission.

Independent Examination

Having created your year end accounts, if your charity’s income is over £25k, you will need your accounts to be independently examined before they can be submitted to the Charity Commission.

There are no specific qualifications required to be an Independent Examiner of charity accounts where the charity’s income is below £250,000. But the examiner must be independent and have the necessary skills and experience. They can’t be a trustee, an employee, a beneficiary, a major donor, or involved with the running of your charity or related to someone who is any of these things.

In terms of skills and experience, the Charity Commission recommends that examiners for charities with an income over £100,000 have a qualification in charity finance or be a qualified accountant.

However, it’s worth bearing in mind that just because someone is an accountant, that doesn’t mean they have any experience of charity accounting or necessarily understand fund accounting.

This can be problematic with some Independent Examiners failing to spot basic fund accounting mistakes, and unable to correctly advise charities when fund accounting questions come up.

Other problems that charities experience include:

- Overpaying for Independent Examination – this can be avoided by getting quotes from 2 to 3 different companies

- Independent Examiners advising charities to use business accounting software – this often comes from a lack of knowledge of fund accounting, and accountants wanting what is easiest for them, rather than what is best for the charity paying them

- Inefficient Examination Process – some examiners require reports and receipts to be manually downloaded and sent to them, rather than simply providing access to the accounting software that contains the data.

Top Tip: You are free to switch Independent Examiners – you don’t need to stick with your existing examiner. We can highly recommend both Wyatt & Co and Stewardship. While we get no benefit from recommending these companies, we do so because both have excellent knowledge of fund accounting, they aim to help churches and charities and have reasonable fees for the service they deliver.

You should choose an Independent Examiner who has an excellent knowledge of fund accounting and who can support you with any questions. Their independent examination should provide your trustees with confidence and assurance that your charity accounts are correct.

Information needed for Independent Examination

In terms of the information your Independent Examiner is likely to need, this will include:

- Your created accounts

- Access to the data from which the accounts were created, e.g. the transactions by account report from your fund accounting software (also known as your General Ledger), or the spreadsheet used to track your finances

- Access to view receipts and invoices for purchases

- Access to view invoices sent, and income documentation for grants, legacies, and large donations received

- Copies of your bank statements (typically it is easiest to download these as .PDF files)

In addition to the above list, your Independent Examiner may require additional information such as:

- Access to minutes from trustee meetings

- Visibility of Gift Aid claims or

- Trustee ID checks.

It may be worth asking your Independent Examiner to send you a checklist of what they need.

The independent examination is typically very quick, since it’s not a full audit of your accounts. However, your Independent Examiner is likely to have other clients also wanting independent examinations at the same time. We recommend you communicate with your Independent Examiner when you are likely to be ready for your accounts to be examined, and check with them what the expected turnaround time will be.

As part of the examination, your Independent Examiner is likely to come back to you with a list of questions. This is a good sign that their examination is thorough. For example, they may spot that the trustees listed in your accounts don’t match with those listed on the Charity Commission. Or they might ask for clarity about a related party transaction. Or they could ask you about the internal financial controls your charity has in place.

Once your Independent Examiner is satisfied with your accounts you can then move on to signing your accounts.

Signing your accounts

Your final draft accounts need to be circulated to your charity trustees for them to review. This is important because your trustees have a collective responsibility for the finances and running of your charity.

For most charities, charity accounts are formally agreed upon as part of a trustee meeting (either online or in person). The decision that the trustees take to approve the accounts is then minuted in the meeting notes.

Once this happens, one of the trustees needs to sign the accounts on behalf of all the trustees. They need to sign both at the end of the trustees’ written report and also at the end of the Asset and Liability Statement.

If your Independent Examiner hasn’t already signed the accounts, they will also need to do this on the relevant page in the template or supply you with their report, which you can then attach to your accounts.

Signatures can be digital (unless your charity’s governing document requires otherwise). Once signed, your accounts are ready to be submitted to the Charity Commission.

Submitting Accounts

Submitting accounts to the Charity Commission is done via the Charity Commission portal. If you don’t already have access to the portal, you will need to establish who in your charity does have access, or contact the Charity Commission to request access.

Uploading your accounts document to the portal is straightforward. It’s worth noting that the Charity Commission takes the opportunity to ask for some other information on your charity as part of the submission process. E.g. the amount of the largest donation your charity received during the financial year, the largest gift your charity has given, how many volunteers it has, the number of paid employees, etc.

If you are using an accounting package like ExpensePlus, then it is easy to find the information needed. Otherwise, you might need to save your submission and return once you have answers to these questions.

About ExpensePlus

Using a fund accounting package like ExpensePlus will enable your charity to manage finances more easily. It will also provide you with a simple and easy way to keep track of funds and many other useful and time-saving features such as online expense management, Gift Aid management and integration, donation reporting, and much more.

It has all of the reports you will need to create accounts on a Receipts and Payments accounting basis.

Creating year end accounts with ExpensePlus couldn’t be simpler, with an inbuilt accounting template, which we have developed with the help of Stewardship. You also have the ability to provide your Independent Examiner read-only access to your online account, making the examination process much simpler.

ExpensePlus is fully customisable, and it comes with free training and brilliant help and support. Visit expenseplus.co.uk to find out more.

ExpensePlus is a cloud-based fund accounting software package designed for churches and charities. ExpensePlus makes managing fund accounts simple and straightforward. It’s used by hundreds of charities and churches across the UK and is rated 4.8 stars (out of 5) on Google with over 1000 user reviews.