Fund Accounting Images

Downloadable fund accounting images that are free for non-commercial use.

Fund Accounting

A form of accounting used by charities, the principles of which ensure that money is spent on (or earmarked for) the specific purpose for which it was given.

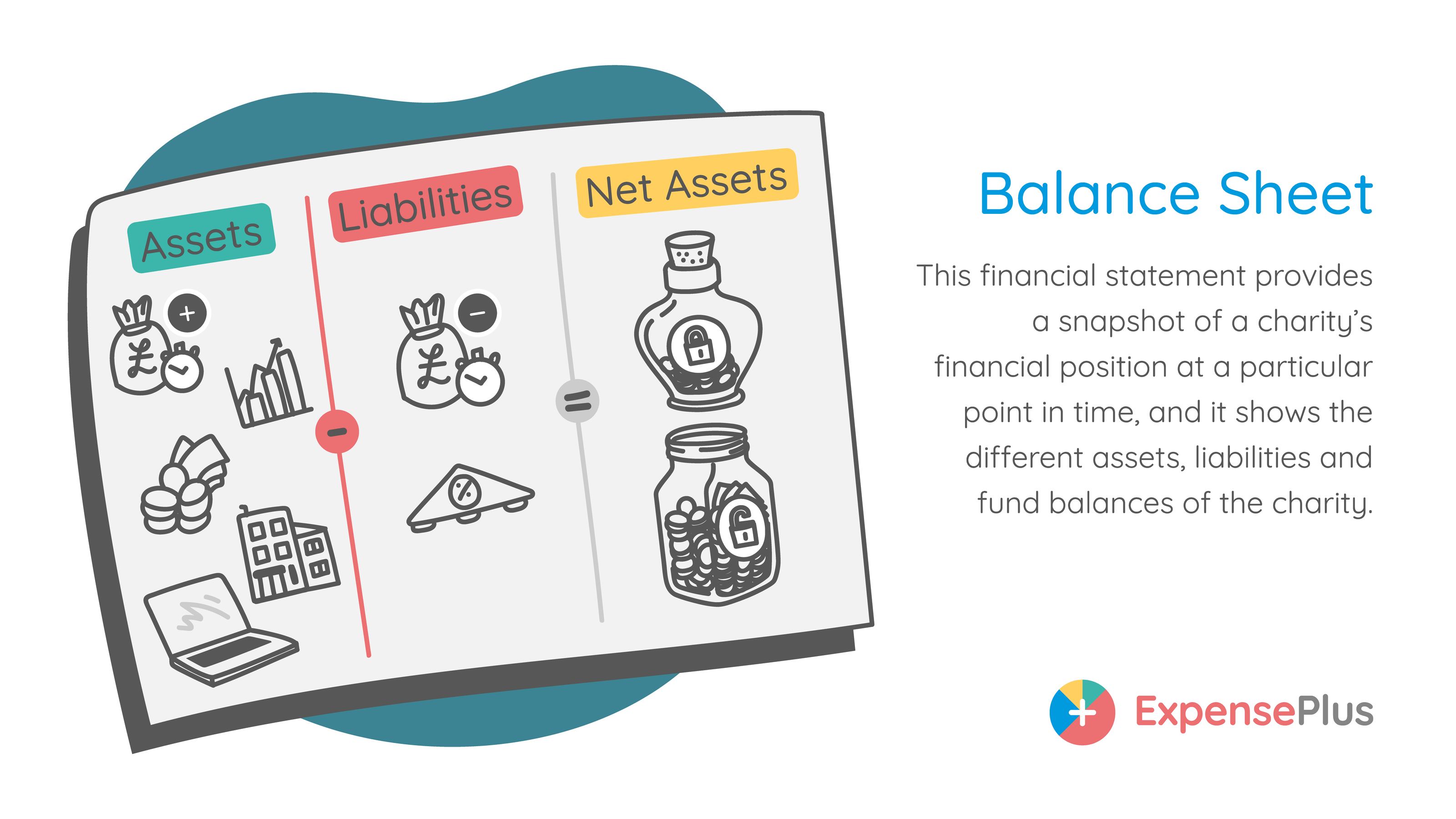

Balance Sheet

This financial statement provides a snapshot of a charity's financial position at a particular point in time, and it shows the different assets, liabilities and fund balances of the charity.

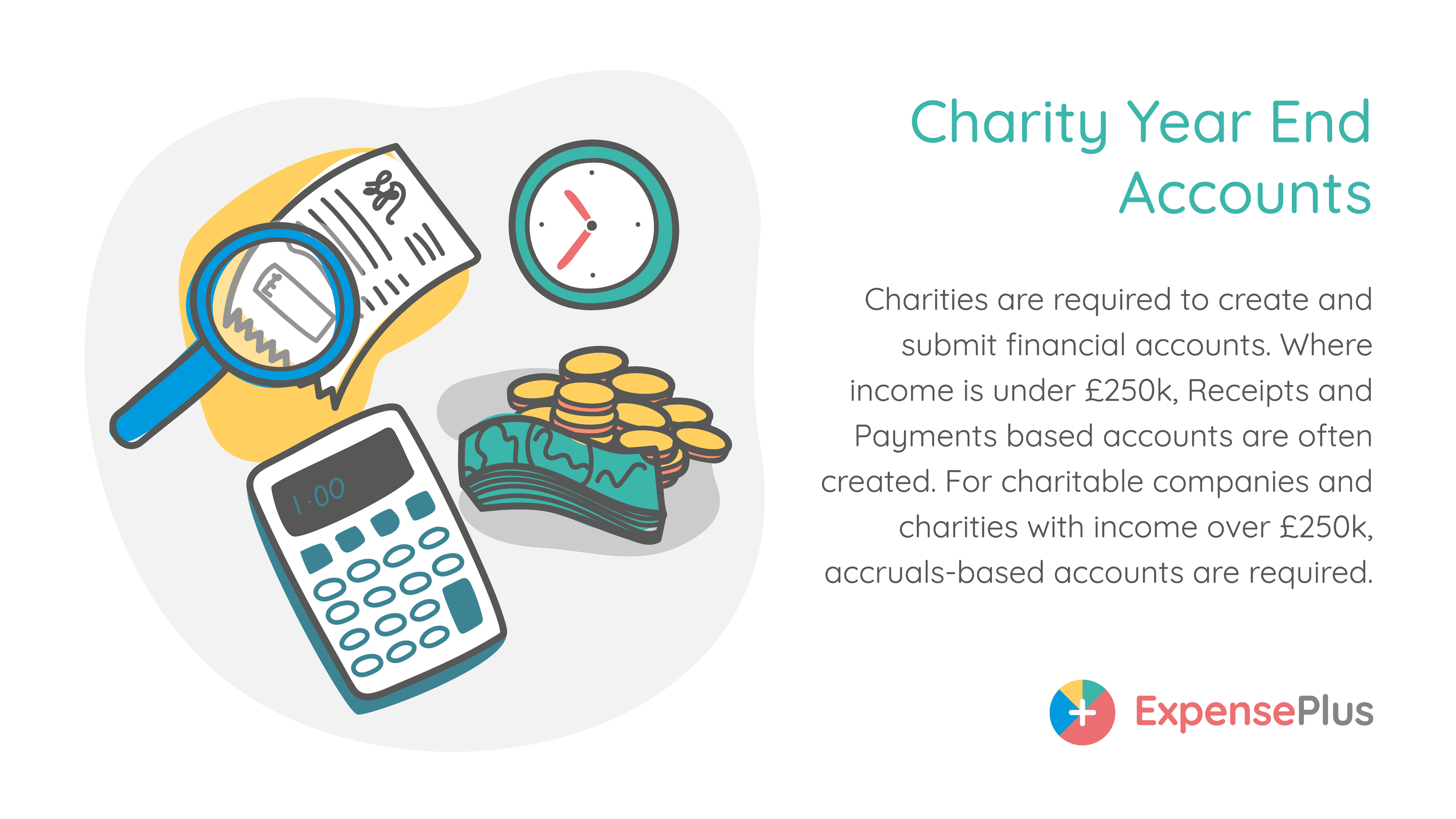

Charity Year End Accounts

Charities are required to create and submit financial accounts. Whilst many charities create accruals-based accounts, smaller charities can often choose simplified Receipts & Payments-based accounts.

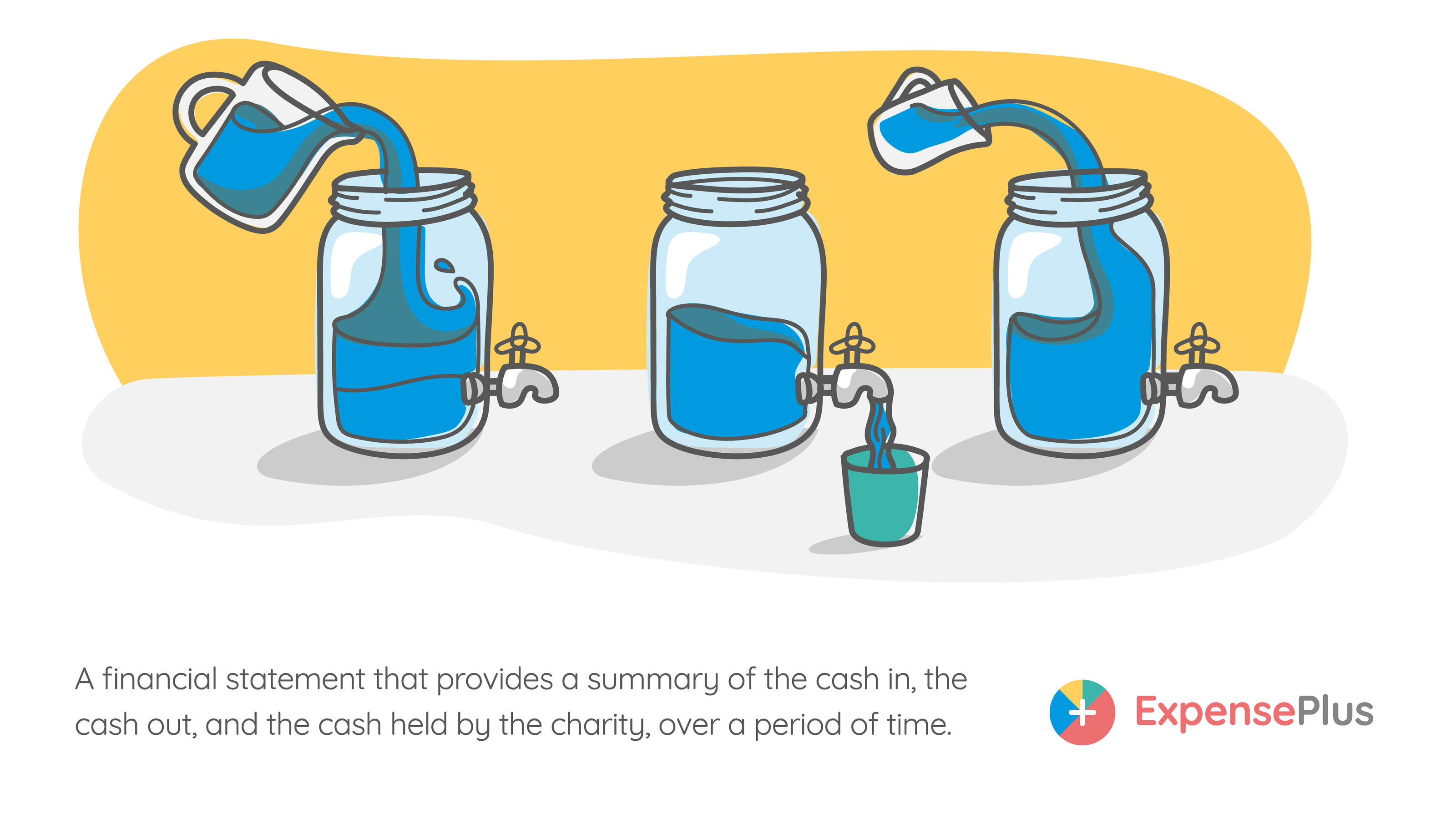

Cash Flow Statement

A financial statement that provides a summary of the cash in, the cash out, and the cash held by the charity, over a period of time.

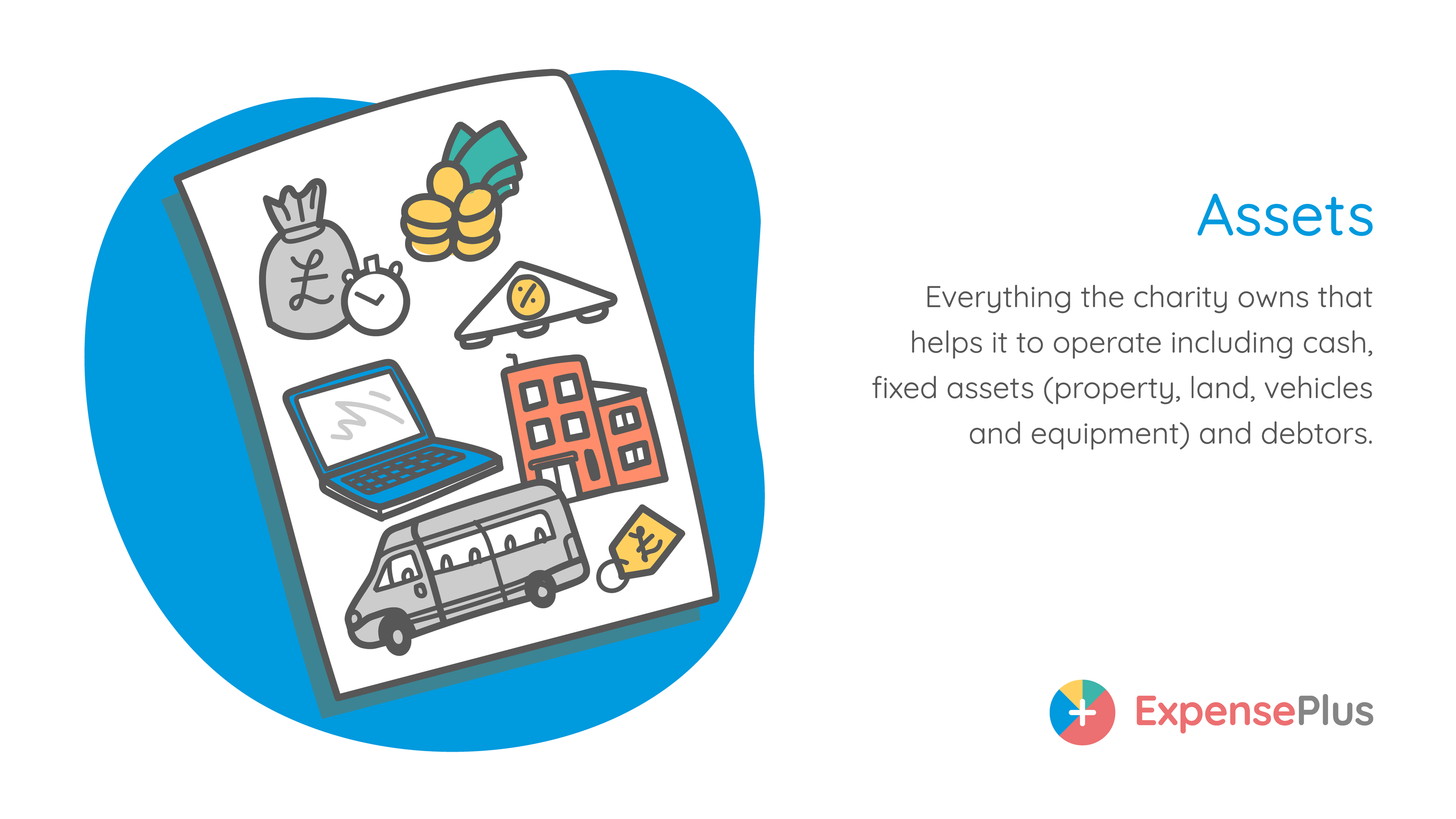

Assets

Everything the charity owns that helps it to operate including cash, fixed assets (property, land, vehicles and equipment) and debtors.

Liabilities

Debts owed by the charity, which can include mortgages and loans, credit card balances, and other money owed (accounts payable). Also included is money received in advance (deferred income).

Income

Money received by a charity or due in.

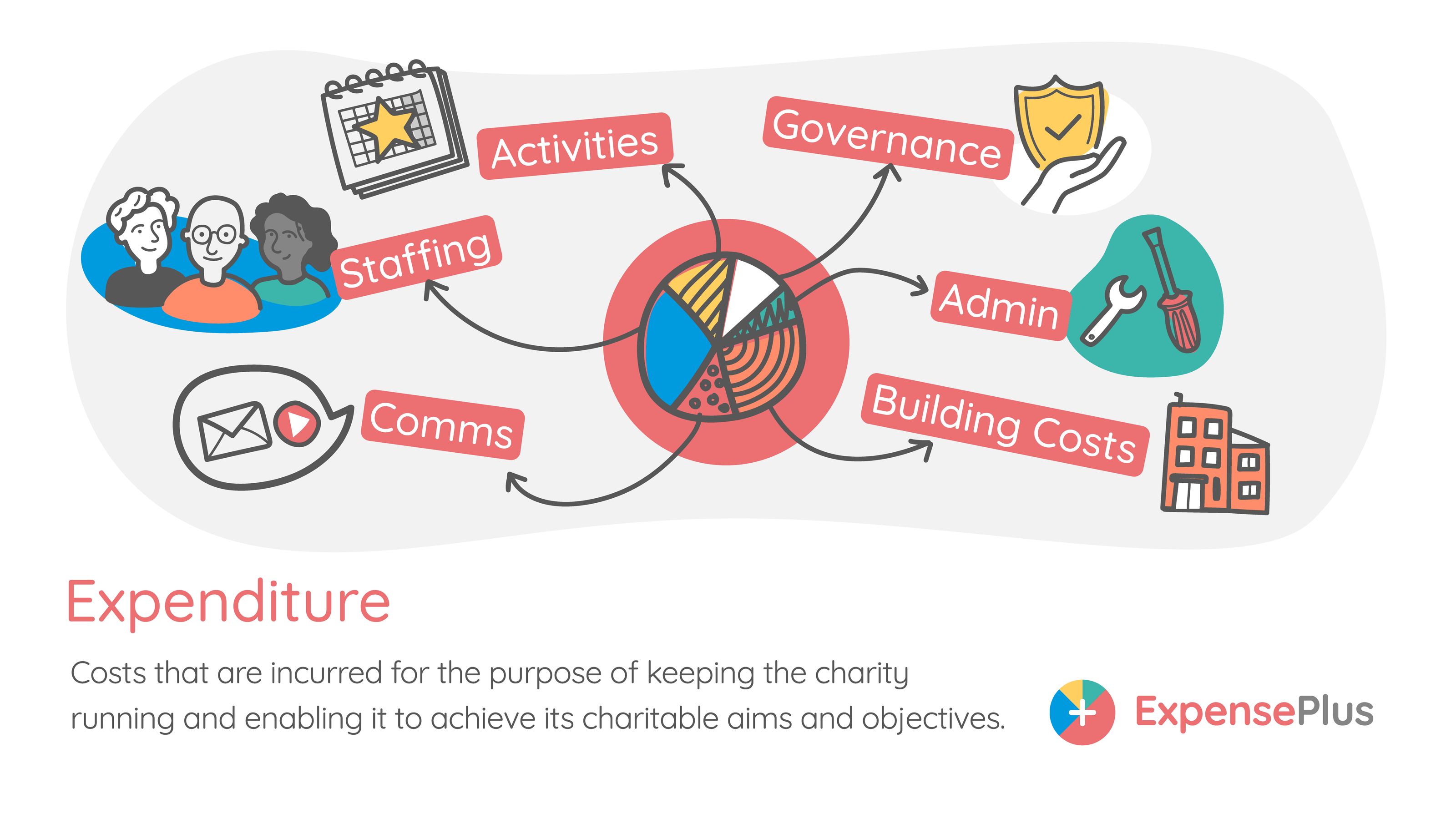

Expenditure

Costs that are incurred for the purpose of keeping the charity running and enabling it to achieve its charitable aims and objectives.

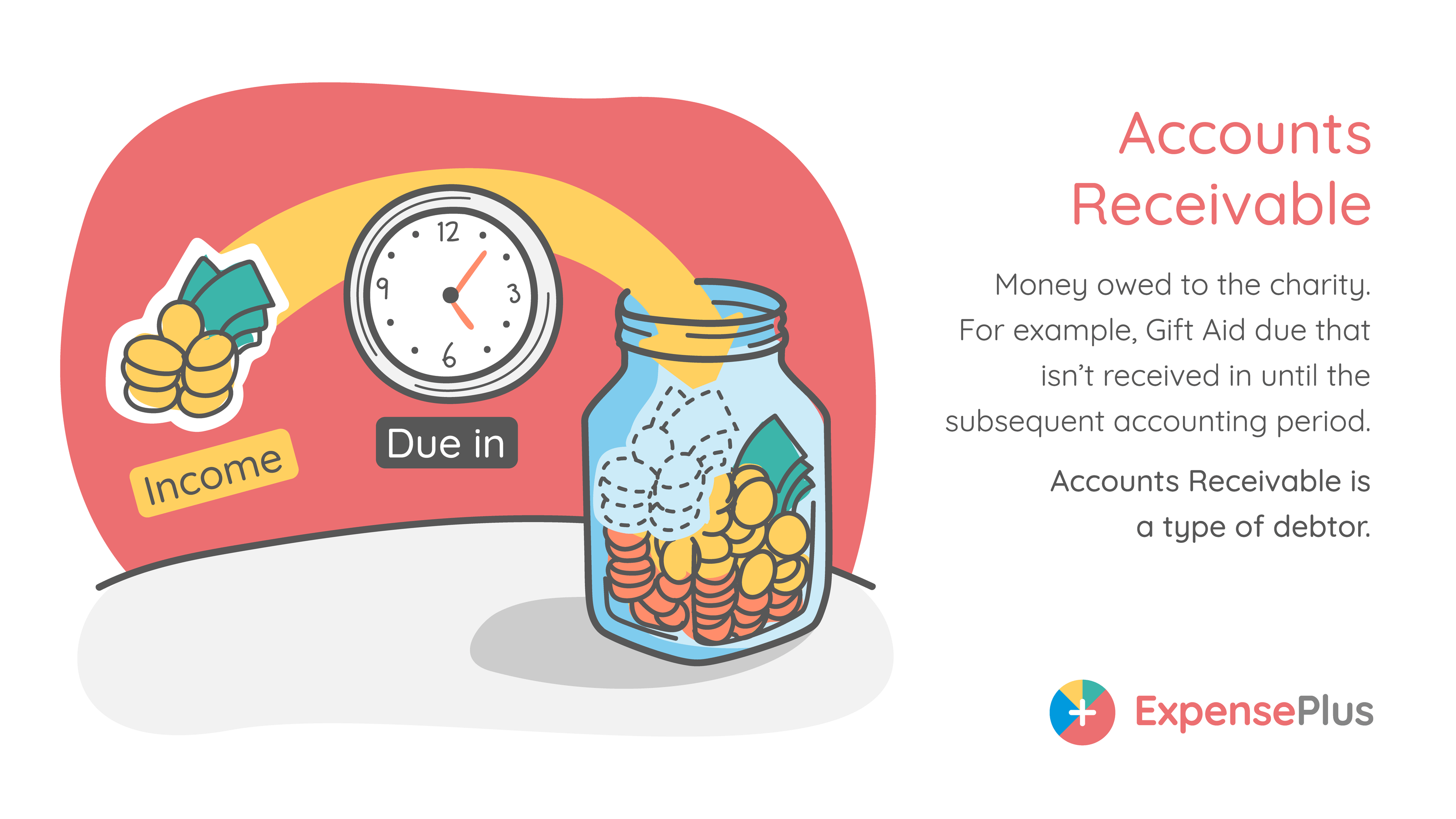

Accounts Receivable

Money owed to the charity. For example, Gift Aid due that isn't received in until the subsequent accounting period. Accounts Receivable is a type of debtor.

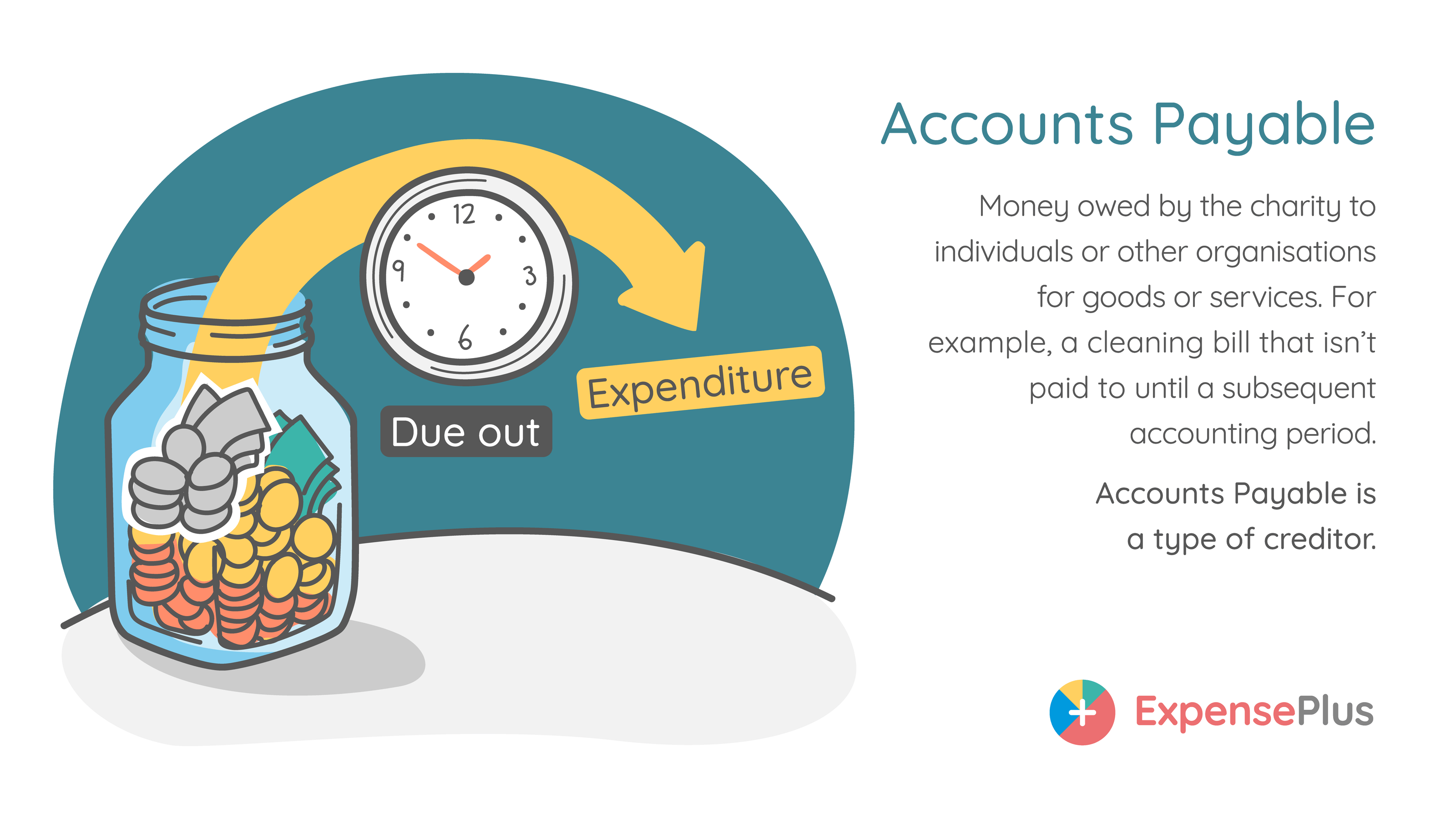

Accounts Payable

Money owed by the charity to individuals or other organisations for goods or services. For example, a cleaning bill that isn't paid until a subsequent accounting period. Accounts Payable is a type of creditor.

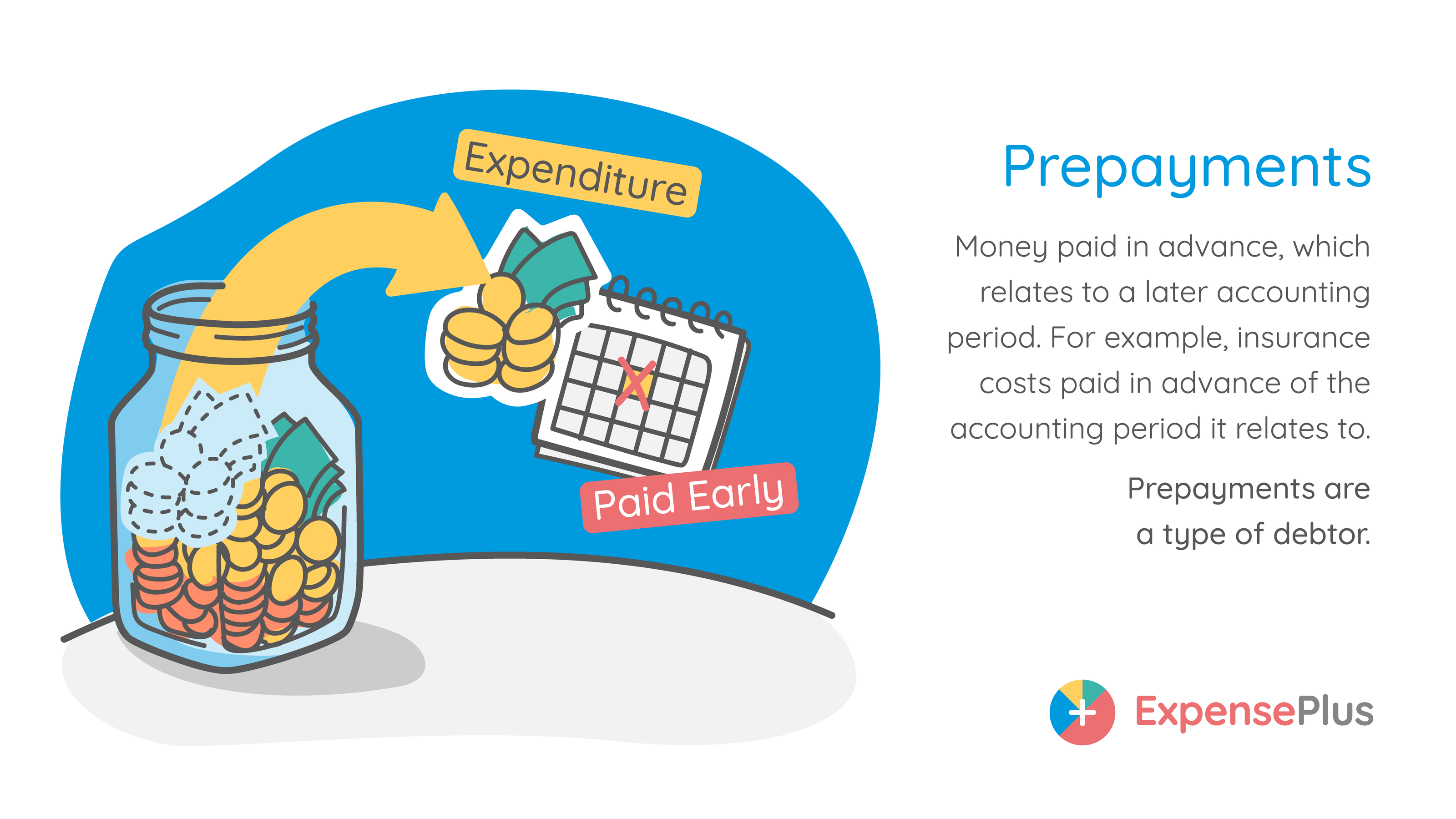

Prepayments

Money paid in advance, which relates to a later accounting period. For example, insurance costs paid in advance of the accounting period it relates to. Prepayments are a type of debtor.

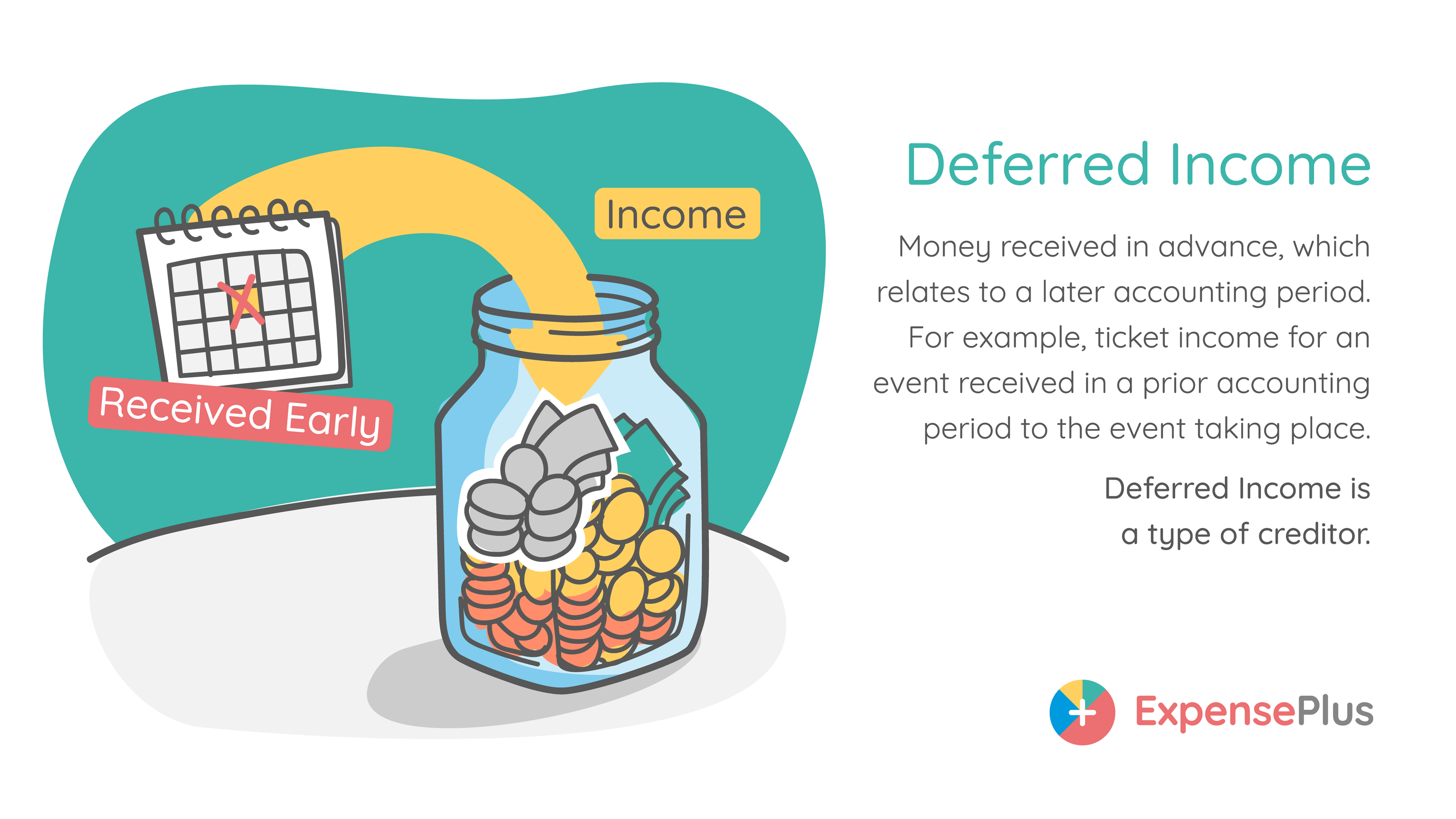

Deferred Income

Money received in advance, which relates to a later accounting period. For example, ticket income for an event received in a prior accounting period to the event taking place. Deferred Income is a type of creditor.

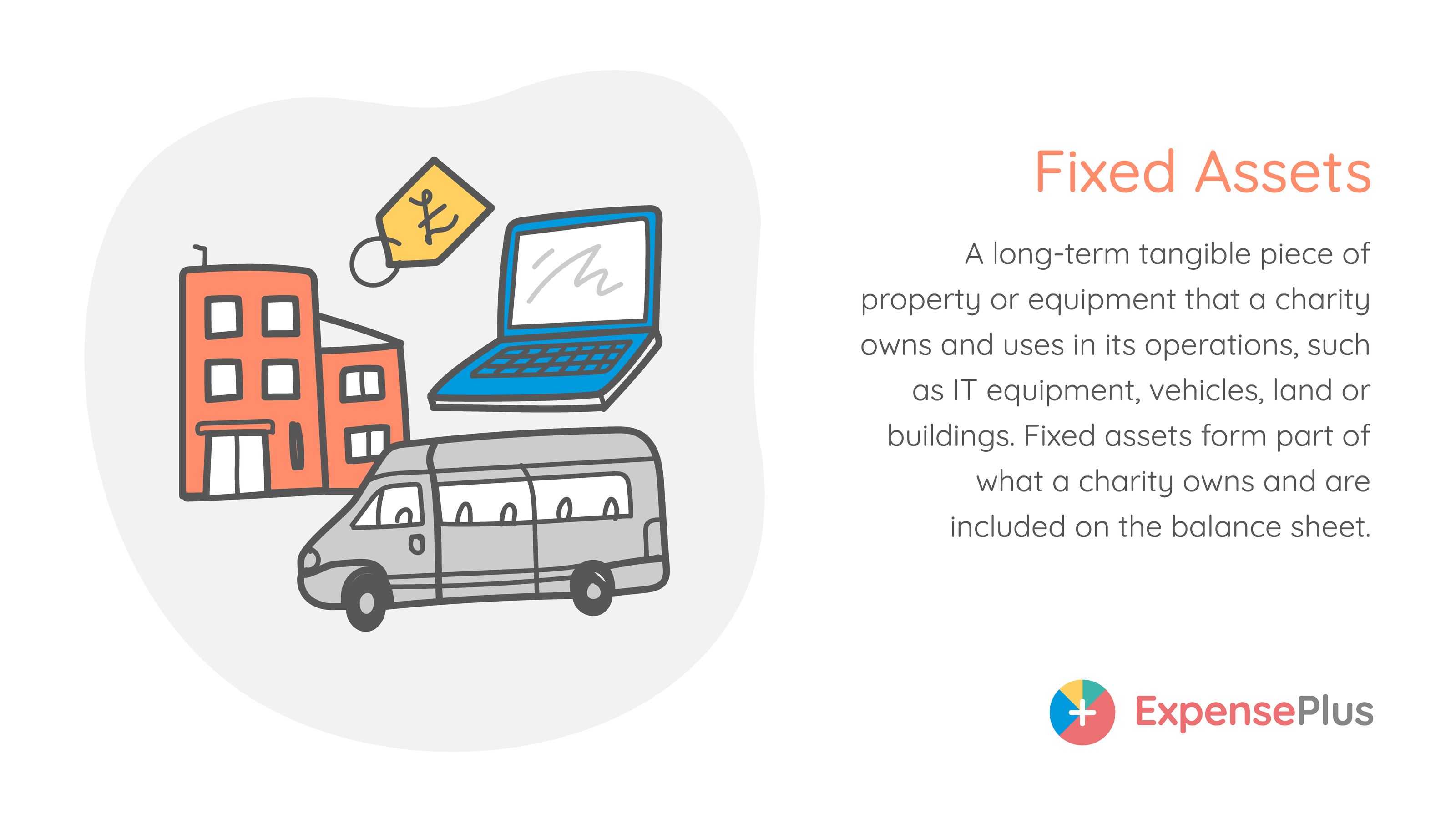

Fixed Assets

A long-term tangible piece of property or equipment that a charity owns and uses in its operations, such as IT equipment, vehicles, land or buildings. Fixed assets form part of what a charity owns and are included on the balance sheet.

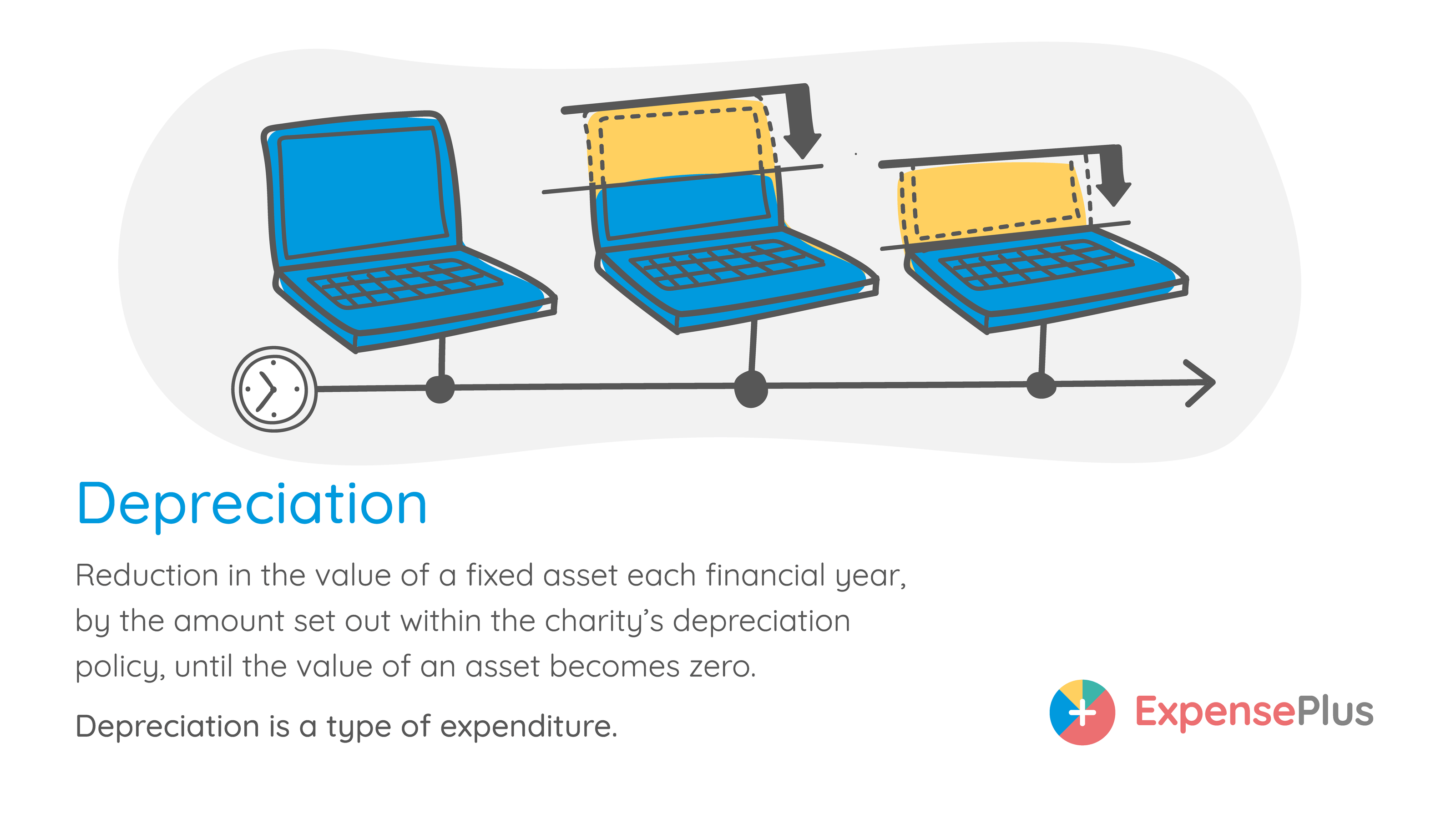

Depreciation

Reduction in the value of a fixed asset each financial year, by the amount set out within the charity's depreciation policy, until the value of an asset becomes zero. Depreciation is a type of expenditure.

Unrestricted Fund

A fund type used for donations and grants received that can be spent by the charity on anything within its charitable aims and objectives.

Designated Fund

This fund type is used when the trustees of a charity decide to earmark / designate / set aside funds for a particular purpose.

Restricted Fund

A fund type used where money has been given for a specific charitable purpose and must be spent on that purpose in line with the donor's instructions.

Bank Account

An account held with a bank or financial institution where money can be deposited, held for a period or withdrawn. In charity accounting, bank accounts are not the same as funds.

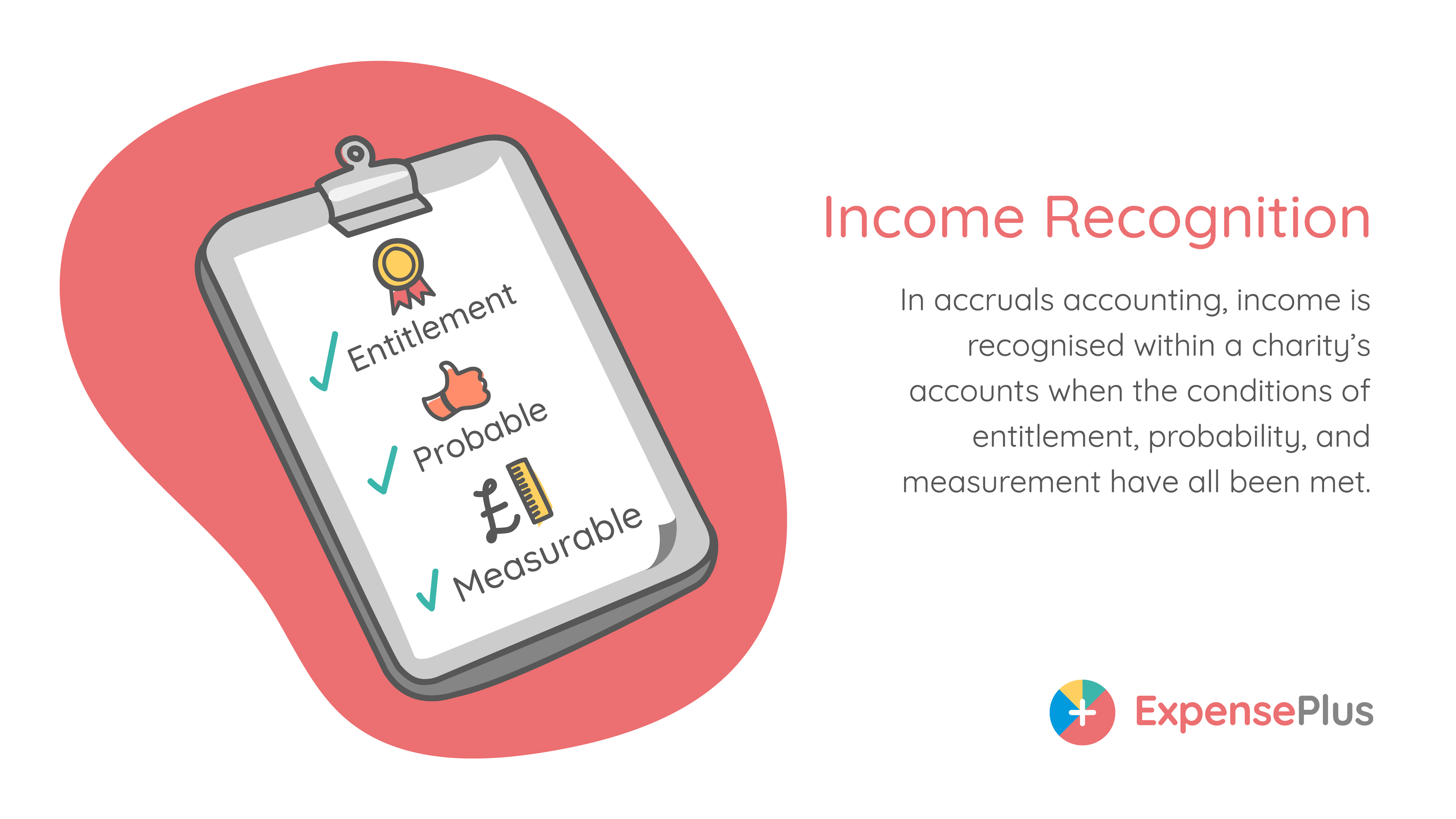

Income Recognition

In accruals accounting, income is recognised within a charity's accounts when the conditions of entitlement, probability, and measurement have all been met.

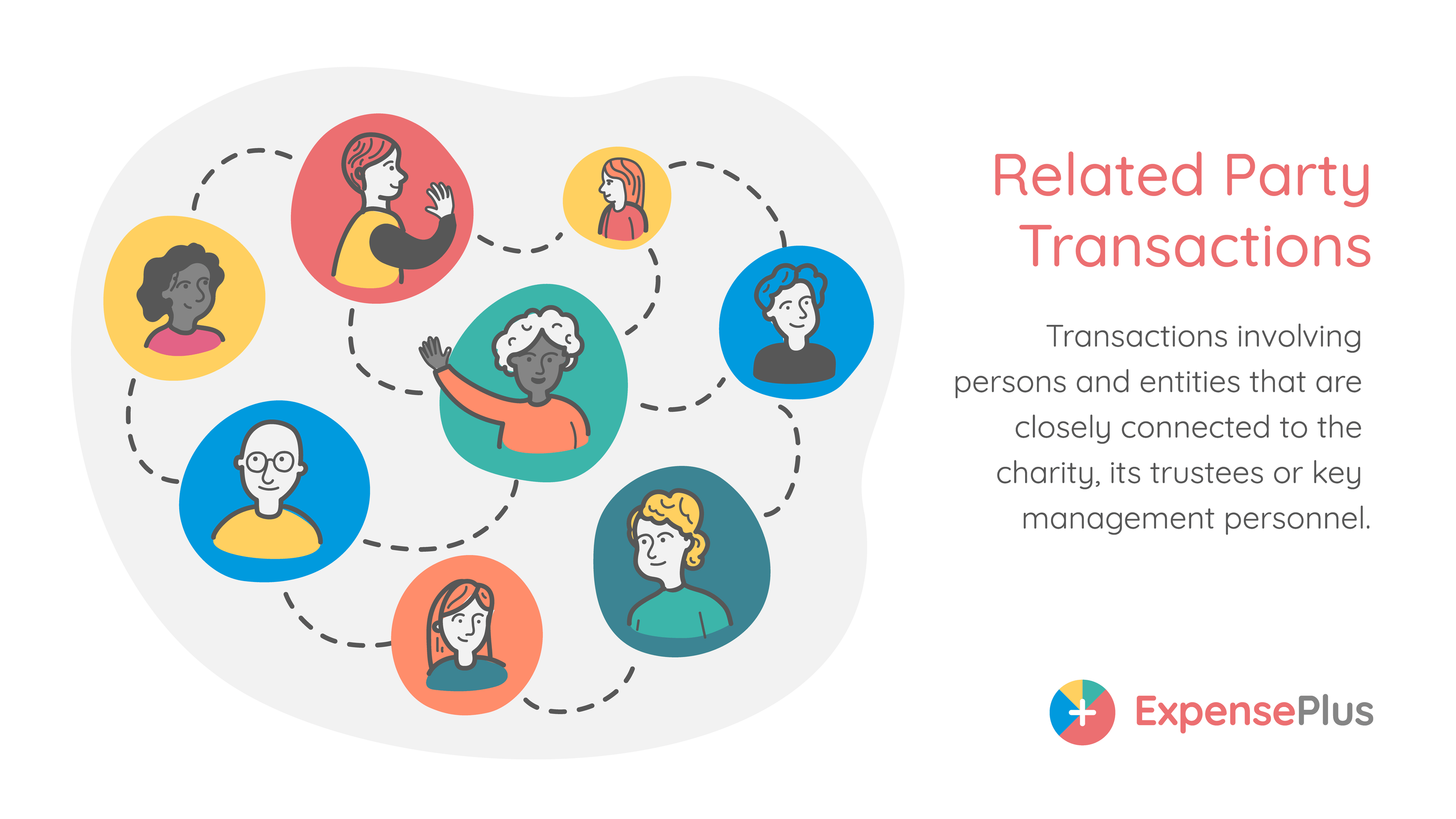

Related Party Transactions

Transactions involving persons or entities that are closely connected to the charity, its trustees or key management personnel.

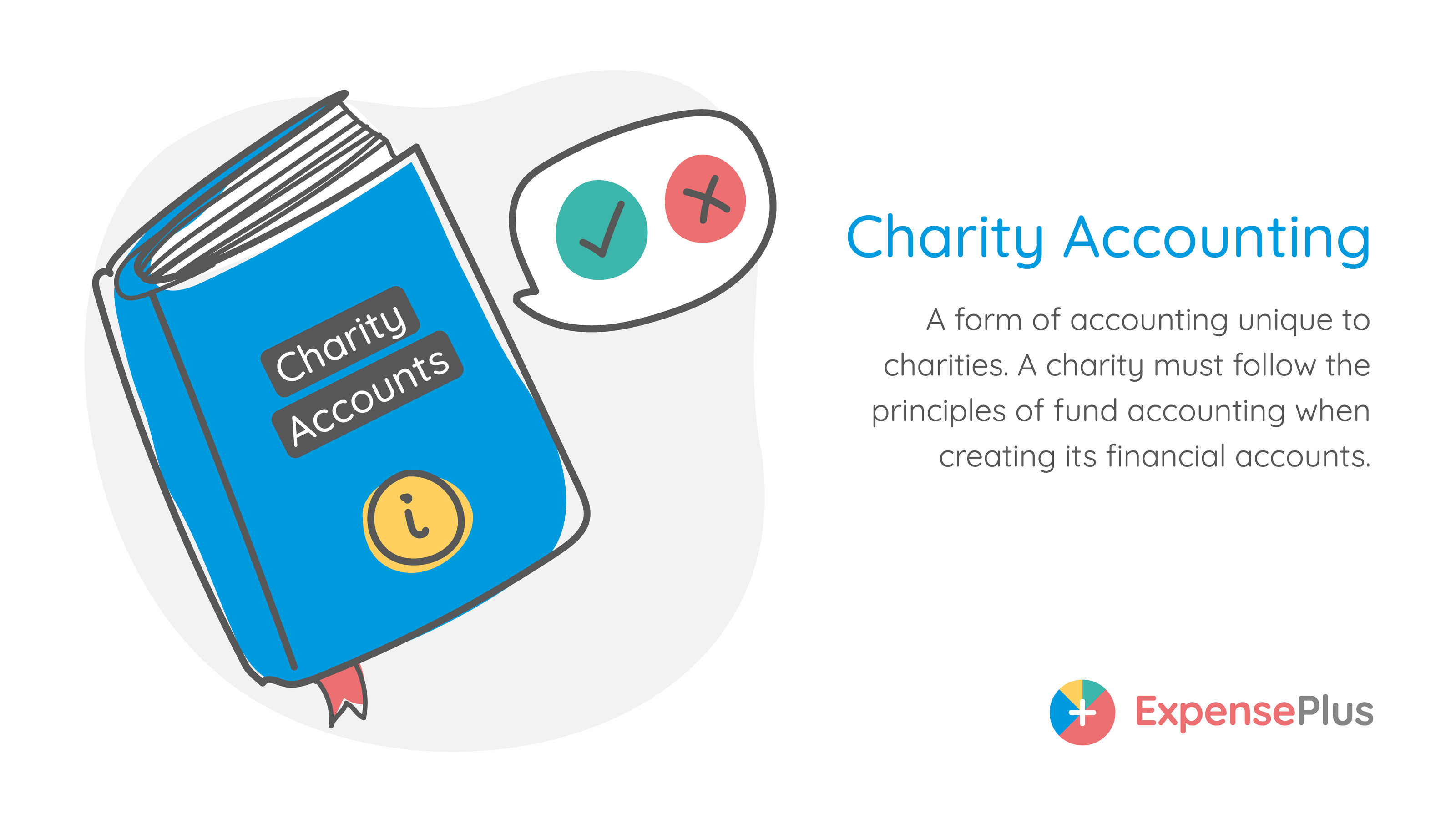

Charity Accounting

A form of accounting unique to charities. A charity must follow the principles of fund accounting when creating its financial accounts.

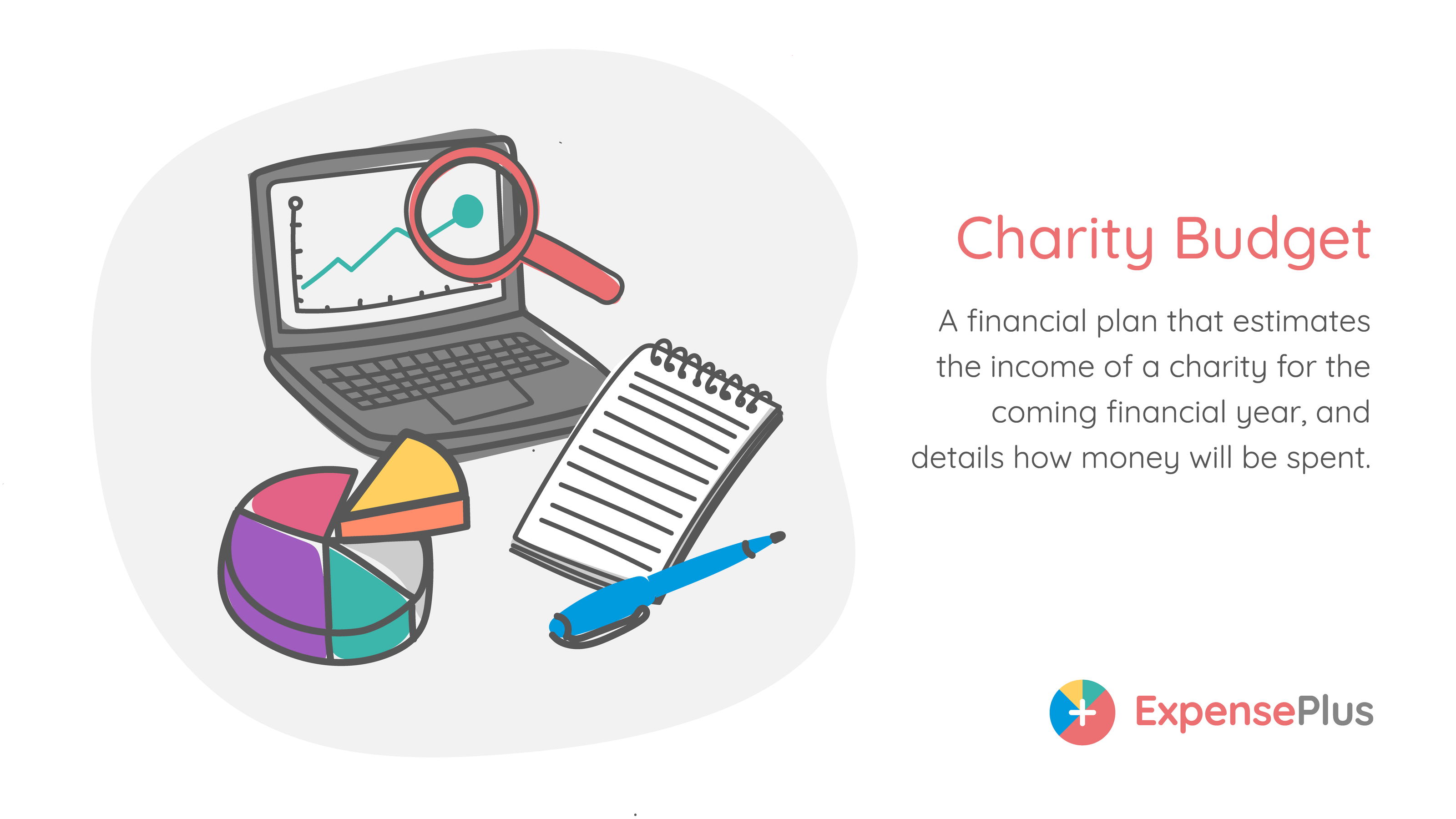

Charity Budget

A financial plan that estimates the income of a charity for the coming financial year, and details how money will be spent.